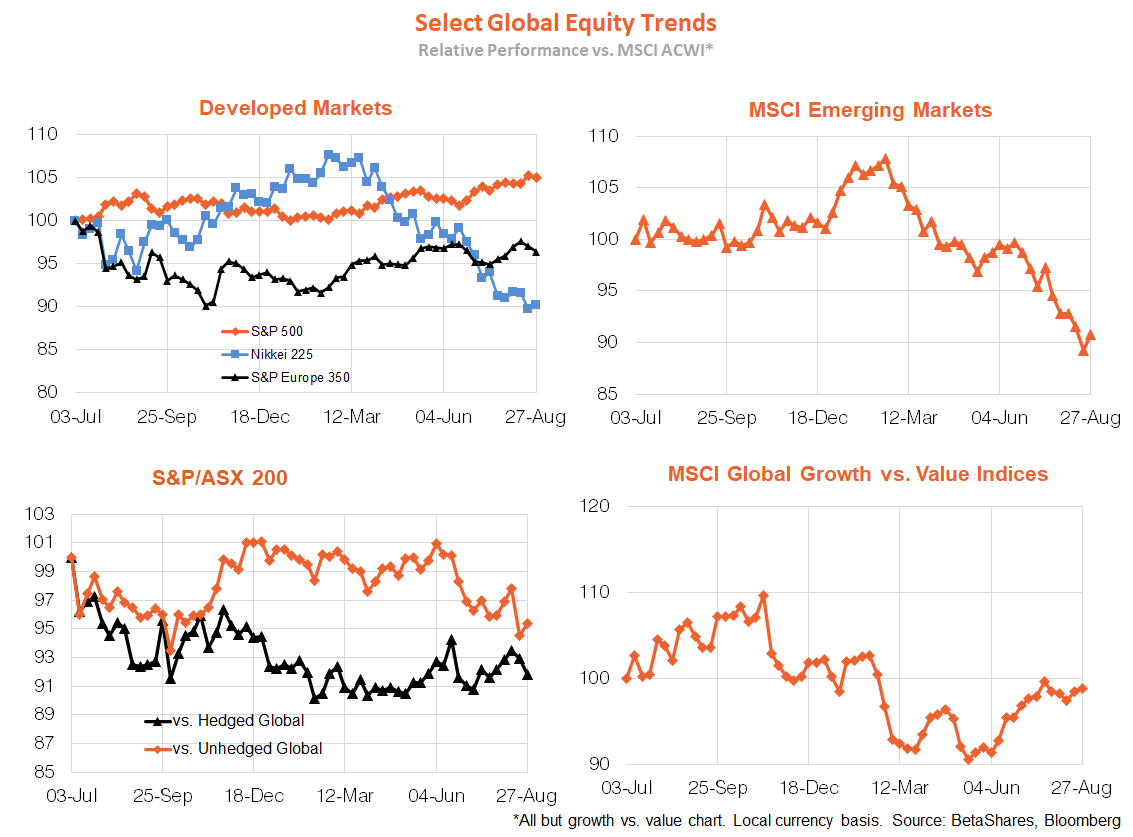

Global markets

Global equities bounced back last week reflecting a relatively dovish speech by Fed chair Powell at Jackson Hole on Friday. The key takeaway from the speech was that the condition of “substantial further progress” towards maximum employment has not quite been achieved, meaning the Fed might still hold off on making its tapering announcement as early as the September 21-22 meeting. After all, there’s only one further payrolls report (this Friday) before the meeting. I suspect Powell was trying to soften up the market further for a likely announcement at the November meeting.

Powell also stressed that there remained “much ground to cover” before he’d even contemplate raising interest rates. While he’s watching carefully, he still suspects the recent lift in inflation won’t be sustained, as more workers return to the labour force and supply-side production bottlenecks are resolved.

The Fed’s dovish signal supported equities and saw bond yields drop, though U.S. 10-year bond yields still ended the week up 5 basis points to 1.31%. The $US eased, after showing some strength in recent weeks, which in turn tended to support commodity prices and the $A. I suspect the recent rally in long-term bond yields has ended, with more range-bound performance now likely over coming months.

Given this backdrop, Friday’s U.S. August payrolls report looms large. The market is anticipating another solid employment gain of around 730k, with the unemployment rate dropping to 5.2% from 5.4% – despite still surging COVID cases in some States over recent weeks. One factor to watch remains wages, with annual growth in average hourly earnings expected to hold at a still relatively elevated 4%, though potentially still being distorted by heavier employment losses among low wage service sector workers over the past year.

In his speech, Powell argued “we still see little evidence of wage increases that might threaten excessive inflation”, though he did concede wage growth had picked up of late (even allowing for compositional shifts) and now “appeared consistent with our long-term inflation objective”. So far so good, but that does not leave much margin for wages to move up further before this inflation objective might presumably be threatened. What will be key over coming months is whether labour force participation recovers (as it usually does with a lag after recessions) and so checks any further untoward rise in wages as the economy continues to re-open for business.

Somewhat reassuringly, Powell also noted that U.S. unemployment ran below 4% for two years prior to the pandemic and, while wage growth did move higher, “not by enough to lift inflation consistently to 2%”. As was the case pre-pandemic, we’re now on U.S. wage inflation watch!

Australian markets

The S&P/ASX 200 Index lifted only 0.4% last week, though should benefit somewhat today from Wall Street’s Friday rally. We did receive a few encouraging GDP building blocks last week in the form of reasonably solid business spending, though flat housing construction. While we’ll learn more from corporate profits, inventories and net exports over the next two days, June quarter GDP growth due out on Wednesday is likely to remain comfortably above zero, thereby reducing the risk of a double dip technical recession (given we know Q3 GDP will be deeply negative).

More broadly, Australia’s two major states remain mired in lockdown, which seems likely to remain the case for several more weeks – until vaccination rates have move up to at least 70% of the adult population.

Have a great week!