Global markets

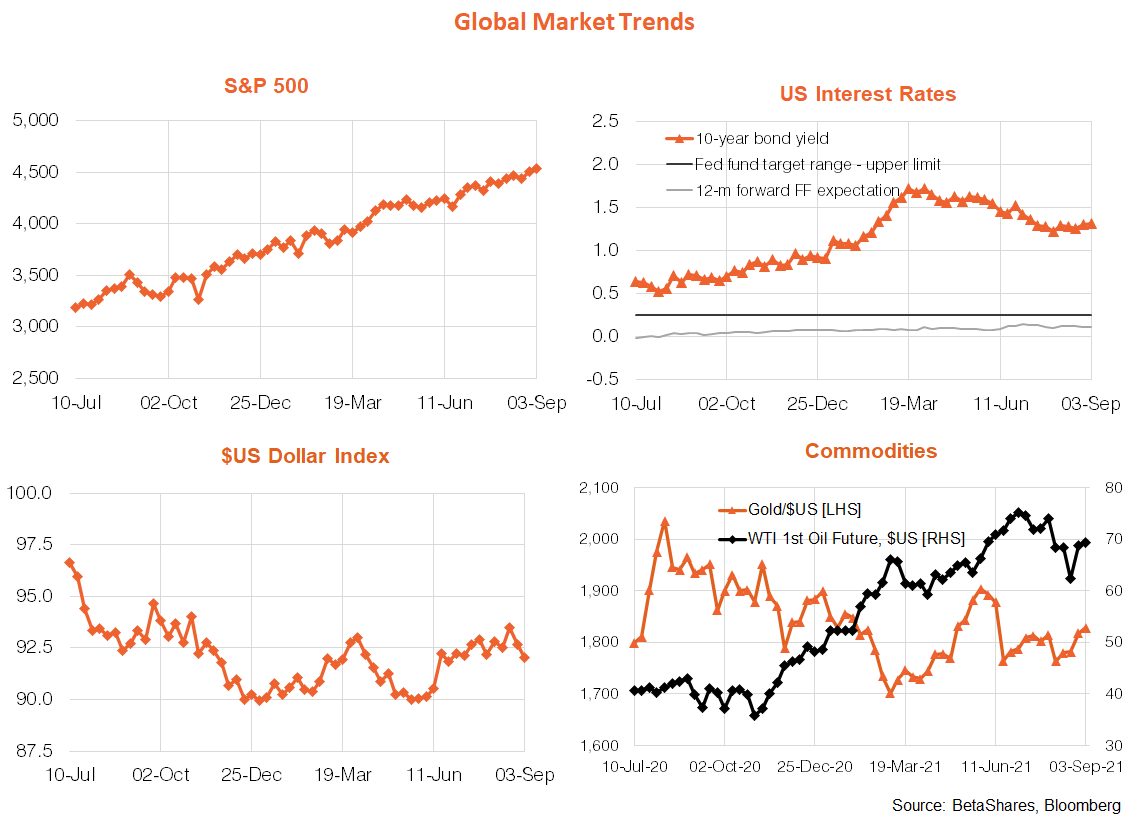

It was a relatively muted week on global markets following the flurry of excitement around the Fed’s taper intentions over the previous week. All up, the story remains that equities continue to grind higher, helped by still solid growth in earnings and broadly steady interest rates. The major highlight again came on Friday with a much weaker than expected U.S. payrolls report, which appeared to reflect both a delta-related slowdown in employment demand and lingering employment supply bottlenecks. Either way, the upshot is the new dose of economic uncertainty likely killed off any chance of the Fed formally announcing taper plans at the September policy meeting, which should further lessen the risk of any untoward rise in bond yields any time soon.

Also of note last week was an encouraging bounce back in Asia/emerging market themes, helped by signs that the region could be getting past the worst of the latest COVID outbreak. The resignation of embattled Japanese Prime Minister Yoshihide Suga clearly helped, which has increased talk of new Japanese stimulus and/or a better COVID response. Chinese August service sector data was also weak, reflecting delta-related restrictions – which in turn has increased talk that China might relent on recent policy tightening.

In an otherwise data-light week, one focus will be what the usual parade of Fed speakers think about tapering in light of last week’s payrolls miss. The European Central Bank’s Thursday meeting might also attract more than usual scrutiny given recent murmuring from some officials suggesting it should also start to think about tapering bond purchases. U.S. producers prices on Friday will also be of interest given the simmering concerns over inflation. All up, however, I don’t expect any of these events to be especially worrisome for markets – with bigger hopeful news being signs of a global cresting in the delta COVID wave.

Australian market

Australia got a rare bit of good news last week with a better than feared Q2 GDP result. As I suspected, given strength in several partial indicators, GDP growth was positive, at 0.7%. Of course, Q3 GDP will be deeply in the red and we still can’t be confident Q4 won’t be negative also until we see more clarity around a post-vaccine easing of restrictions. Either way, the equity market continues, admirably, to look through the mayhem, helped by a still solid global equity outlook and very poor alternative investment choices!

The confluence of events last week – solid local data, weak U.S. data and an improved Asian outlook (as reflected in strong iron-ore prices) helped boost the beaten-down $A – at least for now.

The focus this week will be on whether the RBA delays its planned tapering of bond purchases at Tuesday’s policy meeting. For the record, I think it will delay, not that I think the decision will affect the economy or markets too much either way. Given heightened economic uncertainty, however, it’s just hard to see the RBA blithely proceeding on with a planned policy tightening – though it always retains the capacity to surprise!

We’ll also learn more about the resilience of business sentiment with the National Australia Bank August business survey on Thursday. It’s hard to imagine an especially strong result, though the fact that smaller states outside of New South Wales and Victoria are not in lockdown (much less living in caves) should help at the margin.

Have a great week!