Downward movements in bond yields have supported returns from fixed income products in recent years. But with interest rates now close to record lows domestically and offshore, the scope for bond yields to fall further appears more limited. In turn, fixed income funds might struggle to maintain their strong recent performance track record.

We’re not suggesting bond yields are going to rise meaningfully in the immediate future, but they are likely to rise over time as economic conditions improve. With that in mind, it’s important that fixed income investors and asset allocators are aware of the implications of such a move.

Are we close to the end of a ‘super-cycle’ in bonds?

In Australia and other major markets, bond yields have fallen fairly consistently over the past 20+ years. The chart below shows the yield on 10-year Commonwealth Government Securities; a commonly used yardstick for bond yields in Australia.

Figure 1: Long-term downtrend in Australian bond yields

Australian Commonwealth Government 10-year Bond yield, 1 January 2000 to 30 September 2021.

Source: Bloomberg 1 October 2021.

Bond yields plunged to record lows in 2020 following the Covid shock, a move that can be seen clearly on the chart. Similarly, many investors will remember the significant volatility in yields in 2008 and 2009, when central bank policymakers and global bond markets responded to the Global Financial Crisis.

At times bond yields have risen for short periods, but overall wehave seen a fairly steady one-way trend. This is well represented by the green line on the chart a 36-month moving average of the same 10-year bond yield. This smoothed series eliminates short-term volatility and highlights the long-term trend.

Remember, bond yields and prices are inversely correlated – when yields fall, prices rise; and vice versa. Bonds have therefore provided pleasing returns for investors over the past 20+ years; essentially we’ve seen something of a ‘super-cycle’ in fixed income for more than two decades.

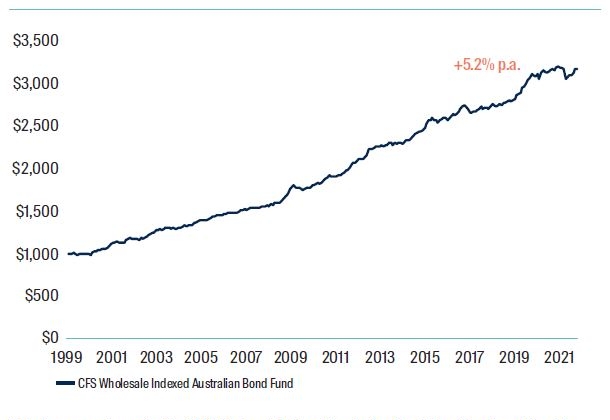

The favourable performance can be quantified by looking at the returns of the Colonial First State Wholesale Indexed Australian Bond Fund1, a passively managed option that aims to match the returns of the Bloomberg AusBond Composite 0+ Year Index – the most commonly-used benchmark for local fixed income products. As bond yields trended lower, Fund returns trended higher. In the 20+ years since inception in 1999, the Fund has generated annualised returns of more than 5%2.

Figure 2: Long-term growth of an investment in indexed Australian bonds

Net returns are shown for the CFS Wholesale Indexed Australian Bond Fund from inception 31 January 1999 to 30 September 2021.

Source: First Sentier Investors 1 October 2021.

That’s great news for investors who’ve held some bond exposure in their portfolios in the past, but what about going forward? How might bond yields move in the future, and how will this affect return expectations from fixed income products? More specifically, could we be close to the end of the ‘super-cycle’ in bonds?

These are important questions, particularly as we’re continuing to see meaningful inflows into fixed income funds in Australia. Investors should understand how potential changes in bond yields will affect these investments.

Potential implications of rising bond yields

Let’s be clear – the 5%+ annualised returns from the domestic fixed income market, which we’ve become accustomed to over the past 20 years, are unlikely to be repeated in the years ahead.

That’s because the performance of the Bloomberg AusBond Composite 0+ Year Index – and, in turn, expected returns from passively managed portfolios – is primarily driven by changes in government bond yields3.

To maintain the favourable performance track record, Australian Commonwealth Government Bond yields would have to continue to fall. But how much lower can they go? They’re already close to record lows, and not too far above zero. It is possible for bond yields to fall below zero – we’ve seen that in Japan and Germany, for example – but in our view this is unlikely to be sustainable over time.

For now, central banks in Australia and elsewhere are supporting economies through Covid-related slowdowns by keeping official interest rates at record low levels. But interest rates and bond yields almost certainly won’t stay this low forever. Market theory suggests interest rates and, in turn, bond yields will start to increase over time as economic activity levels pick up and inflationary forces gather momentum. Nobody knows exactly when yields will rise, or by how much, but we do know that higher bond yields will impede returns from fixed income products.

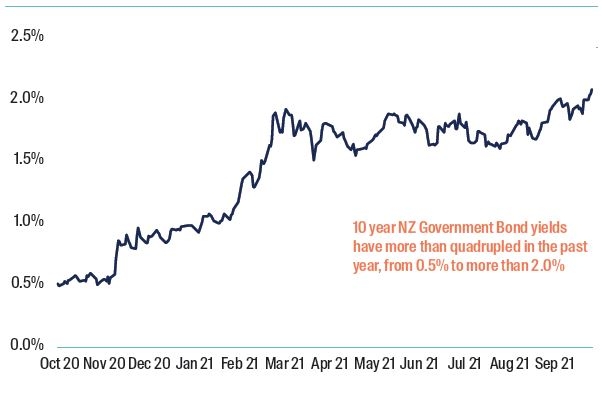

To highlight the point, it’s worth looking over the Tasman, where bonds in New Zealand have been affected by changing interest rate expectations. Bond yields spiked as the Reserve Bank of New Zealand started to talk openly about potential interest rate rises later this year. This resulted in a return of –7.1% from the S&P/ NZX New Zealand Government Bond Total Return Index in the 12 months ending 30 September 20214.

Figure 3: Recent uptrend in New Zealand bond yields

New Zealand Government 10-year Bond yield, 1 October 2020 to 30 September 2021.

Source: Bloomberg 1 October 2021.

Are local income investors prepared for something similar in Australia?

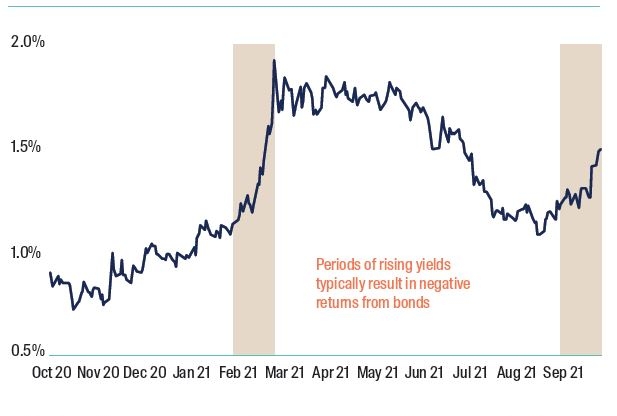

In fact we saw some similar moves earlier this year in this country, amid speculation that the Reserve Bank of Australia might be considering changes to monetary policy settings. Local bond yields rose sharply, resulting in negative returns from the local fixed income market. The Bloomberg AusBond Composite 0+ Year Index fell by 3.6%5 in February alone. This came as an unpleasant surprise for some investors, who perhaps thought that investments in fixed income were relatively stable, and provided capital security.\

Figure 4: Recent moves in Australian bond yields

Australian Commonwealth Government 10-year Bond yield, 1 October 2020 to 30 September 2021.

Source: Bloomberg 1 October 2021.

Australian bond yields retraced most of this upward move in mid-2021, and local fixed income products clawed back their lost ground.

But what about next time, or the time after that, when the increase in yields becomes more entrenched? It’s worth noting that the Bloomberg AusBond Composite 0+ Year Index generated another negative return, -1.5%6, in September 2021 as yields started to rise again.

In our view, an increase in yields seems probable over time as extraordinarily accommodative policy settings start to be wound back, and as official interest rates start to rise. With lockdowns clouding the outlook for the economy and with inflation running below target, the Reserve Bank of Australia has reiterated that interest rate hikes are not on the radar for now. But they almost certainly will be, as and when the economy recovers post Covid. Consensus forecasts suggest the Reserve Bank of Australia will raise official interest rates by the end of 20227. Investors in fixed income products must be mindful of that, and consider whether any changes might be required to their fixed income exposures.

What can be done to mitigate the effects of rising bond yields?

– Consider an allocation to credit, instead of more traditional government-oriented fixed income exposures

As we have explained, increases in yields will adversely affect most traditional fixed income products, as the value of their underlying bond holdings falls. This is not the case with all fixed income options, however, which might be worth bearing in mind given the likelihood of rising yields in the years ahead.

The performance of the First Sentier Wholesale Global Credit Income Fund, for example, is largely unaffected by changes in interest rates and bond yields. Returns from this product are primarily driven by changes in credit spreads rather than movements in government bond yields, as all interest rate risk in the portfolio is fully hedged.

In fact, historically the Fund has performed quite well during periods of rising bond yields. Performance held up well in 2013, for example, during the so-called ‘taper tantrum’, when the Federal Reserve announced it would be reducing the scale of its bond purchases following the Global Financial Crisis. Bond yields rose particularly sharply worldwide at this time. In the 2013 calendar year as a whole, the First Sentier Wholesale Global Credit Income Fund returned 7.0%8 net of fees, compared to just 2.0% from the Australian bond market, as measured by the Bloomberg AusBond Composite 0+ Year Index. We know past performance is not necessarily a guide to future performance; nonetheless, this period highlights how rising bond yields do not necessarily affect credit funds to the same extent as traditional fixed income funds (which favour government and government-related securities).

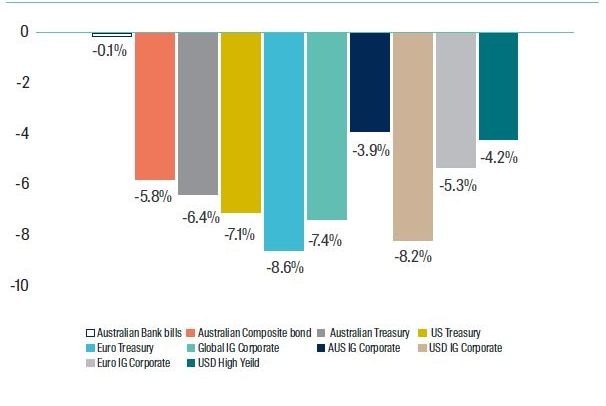

To highlight the point, we’ve simulated the prospective returns from various major global fixed income indices if government bond yields were to increase by 100 bps from current levels. The results are shown in Figure 5 below.

Figure 5: Performance impact of a 100 bps increase in bond yields

Bloomberg AusBond Bank Bill Index; Bloomberg AusBond Composite 0+ Index; Bloomberg AusBond Treasury 0+ Yr Index; Bloomberg US Treasury Index; Bloomberg Euro-Aggregate Treasury Index; Bloomberg Global Aggregate Corporate Index; Bloomberg AusBond Credit 0+ Yr Index; Barclays Global Aggregate Corporate USD Index; Barclays Global Aggregate Corporate EUR Index; ICE BofA US High Yield Index.

Source: Bloomberg 1 October 2021.

As we can see from the orange bar, with a current duration of 5.8 years, a 100 bps increase in Australian Commonwealth Government Bond yields would result in an estimated -5.8% return from the Bloomberg AusBond Composite 0+ Index. As we mentioned earlier, most domestic fixed income portfolios are benchmarked against this index.

The durations of other government bond-oriented indices like the Bloomberg US Treasury Index (in olive, which measures the performance of government bonds in America) and the Bloomberg Euro-Aggregate Treasury Index (in light blue, which measures the performance of bonds issued by European governments) are currently longer, meaning these indices would likely perform even worse in a rising yield environment.

Global credit portfolios that do not hedge out interest rate risk are also likely to struggle if government bond yields start to rise. The light green bar in Figure 5 shows that a 100 bps increase in US Treasury yields would currently result in an estimated -7.4% return from the Bloomberg Global Aggregate Corporate Index. US, European and Australian credit indices would also likely see negative returns, corresponding with their current durations. Even if macroeconomic conditions remained favourable for corporates and if credit spreads were unchanged, the return path of unhedged credit products would likely be dominated by movements in ‘risk free’ rates. Even with a duration of just 0.1 year, domestic bank bills would also likely generate negative returns if bond yields rose meaningfully.

Again, we’re not suggesting government bond yields are going to rise by 100 bps or more in the near future, only that it is important that investors in different kinds of fixed income products understand the likely return profiles in various market environments.

Separately, it’s worth noting that credit products provide many of the same benefits as more traditional fixed income exposures, including regular income and an ability to complement equities and other growth options in a well- diversified portfolio.

– Consider actively managed fixed income options

The increased volume of flows into indexed fixed income products in Australia, over the past year or so, is intriguing. With management fees on indexed funds typically lower than on actively managed products, cost may have been an important consideration. With total returns from bonds likely to be lower than the long-term average, investors might understandably be looking to minimise fees, preserving as much of the underlying index return as possible on a net-of-fee basis. Or perhaps investors are unconvinced about active managers’ ability to outperform fixed income benchmarks consistently over time.

Whatever the reason, indexed fixed income funds expose investors to the return of the benchmark index – good or bad. Consequently those who think interest rates and bond yields could rise over time could consider an actively managed product, where managers have discretion to amend portfolio positioning as market conditions evolve. Doing so can help mitigate the effect of rising yields, and help preserve capital.

One way managers aim to achieve this is to amend the overall duration of a bond portfolio. The duration of a bond measures its sensitivity to changes in yields. Knowing a bond’s duration enables managers to calculate how much its price will change for each basis point (one hundredth of a percentage point) move in yields.

Long duration bonds are most sensitive to changes in yields, and securities with longer durations will therefore underperform those with shorter durations in a rising yield environment. If a manager expects yields to rise, they can tilt portfolios towards bonds with shorter durations in the expectation that these securities will outperform longer-dated equivalents. If they’re right and yields move as anticipated, fund returns should beat those of the benchmark.

Most actively managed bond products also have the flexibility to hold exposure to different areas of the fixed income investment universe. Allocations to credit, for example, might help mitigate the effects of rising bond yields. Additionally, some Australian-based fixed income products – like the First Sentier Wholesale Australian Bond Fund and the First Sentier Wholesale Diversified Fixed Interest Fund – are able to invest offshore as well as domestically. This enables the managers to invest in other bond markets around the world, which might at times have superior return prospects than Australian bonds. Again, by actively managing exposures as conditions change, it is possible to construct a portfolio of bonds whose returns will exceed a traditional fixed income benchmark.

We’re here to help

Nobody can be sure if and when bond yields will rise, or by how much. But some of the savviest investors are getting ahead of

the game, reassessing whether their current fixed income exposures remain appropriate given the limited scope for bond yields to fall further.

As we have outlined in this paper, rising bond yields are an ever-present risk for fixed income investors, and can result in unfavourable return outcomes from traditional fixed income

exposures. Ultimately, the likelihood of an increase in interest rates and bond yields over time in Australia and elsewhere will require investors to recalibrate their return expectations for all asset classes. This could have important implications for asset allocation and portfolio construction more broadly.

One thing’s for sure – these are interesting times! The pandemic has changed the investment landscape and continues to have profound influences on markets. We don’t have a crystal ball, but we are here to help. Your Account Manager is available to discuss the various options available, outline the relative merits of different investment strategies and products, and make informed recommendations about how rising bond yields and other changing market conditions might affect your investments.

So give us a call; as the politicians keep reminding us, we’re all in this together.

Footnotes

- Being passively managed, the CFS Wholesale Indexed Australian Bond Fund essentially tracks movements in the benchmark, without any positive or negative performance contributions from active management.

- To 30 September 2021. Source: First Sentier Investors. Past performance is no indication of future performance.

- The Bloomberg AusBond Composite 0+ Year Index includes a small (<10%) amount of credit, but is primarily comprised of government-related securities.

- In local currency terms. Source: Bloomberg.

- Source: Bloomberg, for the period 31 January 2021 to 28 February 2021.

- Source: Bloomberg for the period 31 August 2021 to 30 September 2021.

- Source: Bloomberg as at 1 October 2021.

- Source: First Sentier Investors. Past performance is no indication of future performance.