by Jonathan W. Hubbard, CFA – Managing Director, Investment Solutions Group and Benoit Anne – Director, Investment Solutions Group

As we enter 2022, there are several key themes that will likely influence the macroeconomic and capital markets environment. The past few years have taught investors important lessons around the notions of both fragility and resilience. While the lives of people and operations of businesses were upended by ongoing waves of the coronavirus, economic activity in many countries has recovered to or exceeded pre-pandemic levels and many corporations have sustained high levels of profitability. However, some countries and companies navigated the social and economic implications of the pandemic better than others. Massive amounts of monetary and fiscal stimulus, no doubt, played a meaningful role in the global recovery, with many wealthy countries leading the way due to better vaccination rollouts and substantial amounts of economic stimulus. And many companies found a way to not only survive, but to thrive while investors around the world bid up assets, from stocks to corporate bonds to real estate. A key question for 2022 will be the ability of markets to remain resilient in the face of waning stimulus, a reshaped workforce and more persistent inflationary pressures.

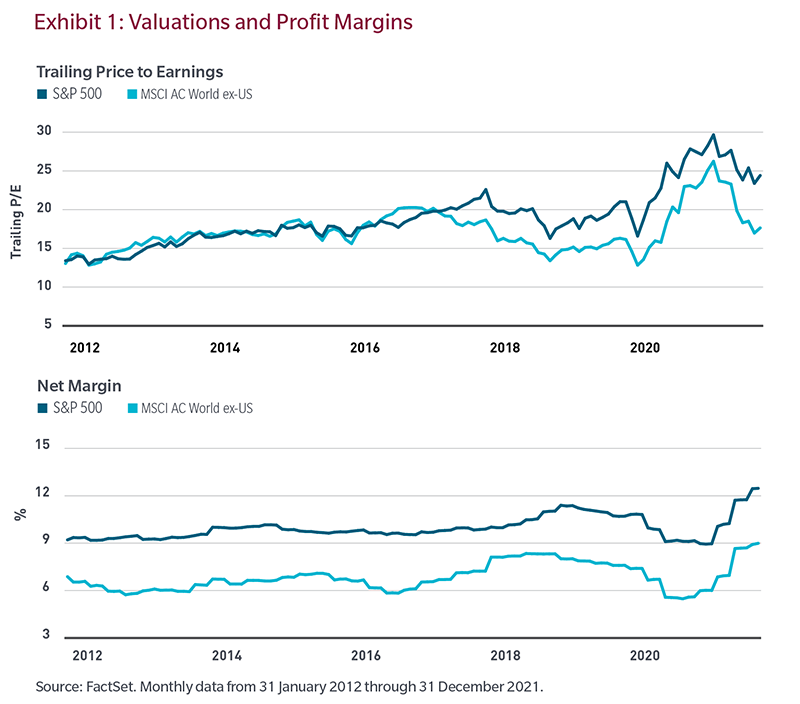

2021 was an extraordinary year for both corporate earnings and profit margins in much of the developed world. Record levels of fiscal stimulus helped keep consumers spending while monetary accommodation kept borrowing costs low and helped support asset prices. While the outlook for 2022 remains solid, we may have passed peak economic stimulus, peak global growth and with that, peak profits margins, at least for now. But corporate profitability, particularly in US large cap companies, has remained robust, allowing companies to reinstitute buyback programs and increase dividend payouts. Despite healthy returns for US and many Non-US equity markets in 2021, robust earnings have brought valuations down on both a trailing and forward-looking basis, although they remain elevated relative to history, particularly in the US market.

Against that backdrop, the environment ahead could prove more challenging for companies that are illprepared for softer economic growth. In addition, supply chain disruptions and inflationary pressures, both of which are proving more persistent than many expected, could eventually lead to demand destruction for some goods and services. Rising wage pressures could also dent margins, particularly considering the shifting composition of the workforce and the renewed strength of labor unions. With employers facing a labor shortage, workers have new-found negotiating leverage, which could reverse several decades of stagnant real wages.

Another newer cost that many companies are grappling with is the cost of implementing sustainability measures. Responding to pressure from shareholders and stakeholders, companies must reckon with a variety of new challenges to bring corporate practices in line with increasing sustainability demands. From cutting back on their use of fossil fuels to reducing their reliance on offshore labor in countries with poor human rights records, these new measures carry financial costs. But done right, organizations that take a holistic and longterm view towards sustainability have the potential to create a long-term advantage over less committed peers.

Investment Implications

- Corporate profit growth may become more scare in 2022, making durable, cash flow generating companies more attractive

- The most attractive companies should be able to effectively navigate supply chain logistics, wage pressures and costs to implement sustainability measures

Central Banks Policy Paths Diverge

Monetary policy actions in 2022 will be key to global markets as central banks across the globe take diverging paths with some remaining accommodative, while many others tighten.

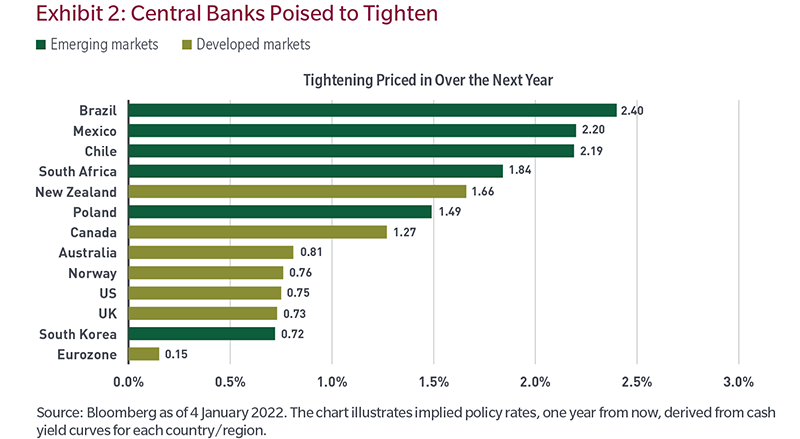

Looking back at 2021, one particularly interesting feature of the global policy cycle was that, for once, emerging markets (EM) central banks led the way on the tightening cycle. Not only was the timing of EM central banks tightening different this time, but so was the root cause. Historically, tightening by EM central banks would often be in response to rising financial stability risks—be it a currency crisis, disruptive capital outflows or unsustainable credit growth— but most EM central banks that engaged in a tightening cycle last year were primarily concerned about the sharp acceleration in inflation, tightening even as the growth outlook appeared fragile.

Across G10 central banks the Reserve Bank of New Zealand, the Norges Bank, and the Bank of England all hiked policy rates while the US Fed engaged in a so-called policy pivot, signaling the forthcoming exit from the Covidrelated policy accommodation. Several other G10 central banks are likely to raise rates this year, starting with the Bank of Canada which may kick off its tightening cycle around the same time as the Fed. We also expect a tightening cycle in Australia, either in late 2022 or in early 2023, while more hikes are also expected in the UK, New Zealand, and Norway.

After recently announcing an accelerated taper, the Fed now stands ready to raise rates for the first time since December 2018, a major development for global markets. Key considerations that could impact markets include: the timing of the first hike; the magnitude of the tightening cycle relative to market expectations, and finally the pace of tightening. Likewise, global investors will need to pay attention to the prevailing global macro environment in terms of the growth-inflation mix, which is a critical input into the Fed’s reaction function. The Fed’s approach to reducing its balance sheet will also require watching.

The risks appear skewed towards the Fed under-delivering on the policy front. There are three hikes currently priced in for 2022, followed by two more hikes in 2023, and a bit more tightening in 2024. The delivery of three hikes may be a tall order, which may materialize only if the US economy remains in full overheating territory. On balance, there is a risk that the Fed falls short, whereas the odds of producing four hikes are low at this juncture. This asymmetric risk has important market implications. This may suggest that the USD may plateau or even possibly reverse in 2022 if the Fed policy moves are underwhelming.

Elsewhere, the ECB and the BoJ will still be fighting for the prize of most dovish central bank in G10. While the Fed will be preparing for its first rate hike since 2018, no policy rate move is on the horizon at either the ECB or the BoJ. While The ECB did announce recently that it would end the emergency funding under the Pandemic Emergency Purchase Programme (PEPP) by March 2022, at the same time, it expanded its regular asset purchasing programme (APP). Overall, it is unlikely that the ECB will consider a rate hike until the latter part of 2023 at the earliest. The story is similar in Japan, where the inflation outlook – stuck near 0% for the foreseeable future—does not warrant any policy action any time soon. The People’s Bank of China (PBoC) will likely strike a different chord this year, easing its monetary policy stance in the face of slowing consumer spending and a liquidity crunch in some sectors. The PBoC already cut its Reserve Requirement Ratio in December, but more forceful action may be in the pipeline over the next few months.

Investment Implications

- Expect central banks to take divergent paths based on the idiosyncratic economic factors in each country or domain, which may create opportunity for active positioning in fixed income

- Many G10 central banks appear likely to join the emerging market counterparts in raising policy rates in 2022, lifting shorter term yields

A Labor Force Reshaped

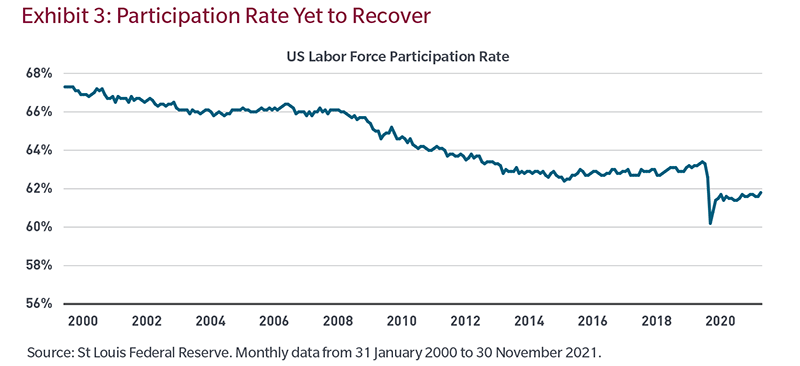

The pandemic forced an abrupt break in work routines and career momentum, leading many workers to reassess their positions. This resulted in a record number of workers quitting their jobs in what is being called “The Great Resignation”. At last count, the US labor force is smaller by about 2.4 million workers compared to February 2020, according to the US Department of Labor. Some workers are reluctant to come off the sidelines due to child-care needs, or hesitancy to return to a communal workplace while others are simply finding better employment opportunities or opting for early retirement. For those working from home – estimated to be about 25% of the US labor force – the line between work and home life has blurred resulting in some workers feeling like they were living at work, rather than working from home. On the flip side, other workers have been more effective at maintaining a better work-life balance, eliminating their commute, and increasing their productivity through technology. While the exodus from offices in March 2020 was abrupt and widespread, the return to offices appears to be much more complicated. A key question facing employers is whether these changes in the workforce are cyclical, or structural. If they are cyclical, what is the path back to normal and when does that journey begin – if they are structural, how should companies change their operations to remain not only functional, but competitive? While the answer is unclear, it appears likely that at least some of the changes are here to stay.

Investment implications for 2022

- Companies will continue to experiment with hybrid work strategies, which is likely be an ongoing, iterative process

- Companies may shift to smaller office infrastructures or regional offices

- Companies may experience increased labor turnover and face demand for higher levels of compensation and better benefits

Inflation May Stay Elevated, But Off Peak

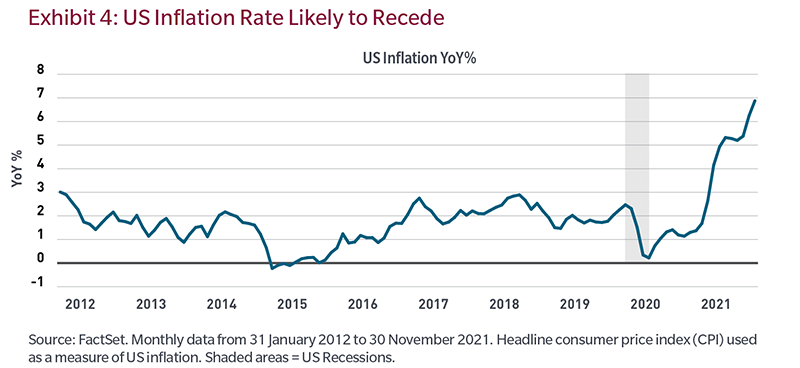

After nearly a decade where inflation rates drifted sideways, a confluence of government stimulus payments, pent up consumer demand, supply chain disruptions and rising energy costs pushed up inflation rates significantly across most developed and emerging economies in 2021. However, we believe the combination of moderating global economic growth, central bank tightening and waning fiscal impulses should lead to decelerating inflation rates in 2022. Industries that experienced the most acute price increases, such as autos and semiconductors, should see price declines from 2021’s sharp increases, but the extent of the decline will depend on how quickly labor, manufacturing and supply chains normalize. While higher goods prices can result in demand destruction, high asset prices, such as those currently seen in equities and real estate, can increase consumer tolerance for higher goods prices, further feeding the inflationary cycle. The result is that inflation may remain stubbornly above central bank targets for the near term, though below recent peaks.

Investment Implications

- Asset classes such as commodities and other real assets have typically been resilient during inflationary periods

- Certain investments, such as longer duration bonds or equities of companies that lack pricing power, may be vulnerable if inflationary pressures persist

Supply Chains Kinks Persist

Since the 1990s, the US and other developed countries have become increasingly reliant on global supply chains to source cheap labor and materials to keep prices down. That strategy worked well until the pandemic unexpectedly shifted consumer demand from services to goods and rolling lockdowns upended wellestablished logistical operations. Companies around the world are now battling supply chain kinks and bottlenecks that have pushed shipping costs higher around the world.

Outbreaks of the Delta variant worsened supply chain turmoil in 2021, especially in Asia, causing computer chip and other factories to shut down, while Omicron and other potential COVID variants are creating longer-term uncertainty. Supply chain woes have exacerbated several other factors, including a shortage of workers in Asia to produce goods and a shortage of truck drivers in the United States to move them. The supply of critical goods such as semiconductors and items that require them as components, appears likely to remain constrained. Making matters worse, some companies may be double-ordering to stock up on hard-to-source materials and components, further boosting demand.

While the second half of the year may bring some relief as supply and demand find their equilibrium, challenges to the supply chain seem likely to persist enticing some companies to bring offshore operations onshore. While not everything will be produced in the US, American companies may increasingly look to source materials from neighboring countries such as Canada and Mexico and upgrade to their supply chain technology, so they are less susceptible to disruption in the future.

Investment implications

- Supply chain disruptions, labor shortages and resulting inflationary pressures may run for far longer than expected

- Identification and recognition of supply chain fragility and their reliance on cross boarder operability may cause a shift to reshoring or regionalization of operations

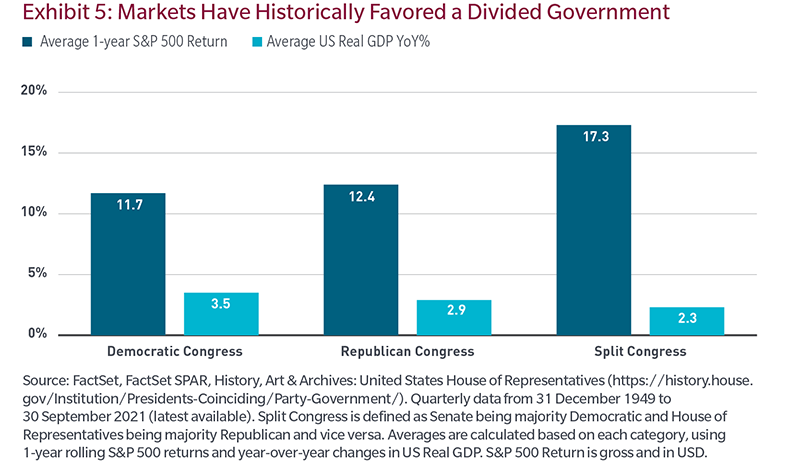

Divided Government May Be on the Horizon

Since World War Two, the party of the sitting president of the United States has lost seats in the House of Representatives in every off-year election but two, losing an average of 25 seats. In those rare instances when the president’s party added seats, the chief executive commanded job approval ratings of 65% or higher in the run-up to the mid-term vote.

While there are many months until the November 2022 mid-term elections, the Real Clear Politics average of polls shows President Joe Biden’s approval rating at 42%, suggesting Democrats will struggle to retain control of their slim majority (221 to 212 Republican seats) in the House and the evenly split Senate. Surging inflation, lingering concerns over COVID-19 and congressional redistricting that should favor Republican candidates this cycle will add to the challenges that Democratic candidates face in the fall. The two most recent Democratic presidents, President Clinton and President Obama, lost 52 and 63 seats in the 435 seat House, respectively, in their first midterm elections (both men served two terms) losing control of the chamber.

While voters might find Washington gridlock frustrating, investors historically have tended to welcome divided government. History shows some of the best periods of returns come when one party controls the White House and the other party controls at least one house of Congress. As the year progresses and the election campaign kicks into gear, major legislative initiatives will have a hard time gaining traction, so we expect Democratic lawmakers will try and advance as many of their priorities in the first few months of 2022 as a possible, such as Biden’s Build Back Better agenda of social programs and infrastructure initiatives.

Investment Implications

- Democratic spending, including and fiscal stimulus, will face a higher hurdle with potentially fewer seats in Congress

- Key initiatives of the Biden Administration, such as investment in green initiatives and free education and childcare could be significantly altered or blocked Increased Regulatory

Scrutiny on Cryptocurrencies

Cryptocurrencies certainly captured the attention of investors over the past year with relentless media coverage and social media chatter. Cryptocurrencies are financial instruments that many see sitting at the center of money, investing and technology, however they have in many respects, lived outside of an appropriate regulatory framework. SEC Chair Gary Gensler has referred to the space as the “Wild West” and Congress held hearings in late 2021 with exchange executives as they attempted to better understand this new technology. The rapid evolution and decentralized nature of cryptocurrencies has resulted in a financial ecosystem rife with opportunities for abuse. One of the many challenges in regulating the digital asset space in the lack of jurisdictional clarity – not only across borders but also across regulatory agencies within those countries. In 2022, expect regulators to find more jurisdictional common ground and work collaboratively to better regulate cryptocurrencies. In 2021, there were several enforcement actions and multi-million-dollar settlements in the crypto arena and regulators are just getting started. Regulators have already started to lay the groundwork for regulations specific to cryptocurrencies. This includes recommendations made by the President’s Working Group on Financial Markets and clarification on crypto exchange requirements by the SEC. Next, we could see know your customer/anti-money laundering enforcement, stable coin bank regulation and requirements for crypto promoters. Better regulation should ultimately be beneficial to cryptocurrencies providing greater transparency, integrity, and efficiencies to the crypto ecosystem. While it appears that cryptocurrencies are here to stay, their ultimate use case remains unclear. They are ineffective as a currency and don’t create economic value, but perhaps clearer regulations will help them find their niche.

Investment Implications

- Greater regulation may help shift from cryptos from a speculative investment to a yet to be defined niche

- As a tighter regulatory framework is built, cryptocurrencies and their providers will lose the ability to engage in the regulatory arbitrage that has allowed them to grow so quickly

- Expect a tighter leash

We continue to strongly believe — as these and other macro and market themes unfold throughout the year, and indeed in any market — that investors should stay diversified across a variety of asset classes and regions and seek to ensure that portfolios are properly aligned with their investment horizon, investment objectives and tolerance for risk. As markets demonstrated in 2020 and 2021, its not only macro and market factors that impact asset prices, but also the reaction function of governments, corporations and investors to those factors that are also key determinants in the direction of the markets.