In my role as Research Analyst for Corporate Connect, I have just released a report giving an in-depth assessment of the present state of the global biotech sector and, in particular, two ASX-listed biotech stocks Corporate Connect currently covers: Antisense Therapeutics (ASX: ANP) and Kazia Therapeutics (ASX: KZA).

In this report, I also provide some insights into what to consider when making an investment in this space that may be of interest, even if the report in its entirety is not.

Those insights are as follows, edited for brevity and context.

…………

There is nothing more alluring to an investor than a stock chart pointing in a northerly direction and nothing more repelling than one pointed in a southerly direction. The real question, however, is are you buying value? The direction a stock chart is headed in is not going to tell you much, if anything, about the underlying value of the asset you are buying.

Drug development is inherently risky and despite what any CEO says every New Chemical Entity (NCE) has approximately a 6% to 7% chance of making it through a phase I clinical trial to market launch and a 14% to 15% chance of making it from phase II to launch [1].

It is only when a drug reaches phase III (pivotal trials) that the chances of getting to launch favour the NCE at 62% or 63%, based on the most recent data. There are only two ways you can improve these odds.

- Diversify Your Holdings

If you have one investment in one biopharma that has one drug with a 50% chance of making it to market you will be either rich or broke. Continue to do this and sooner, rather later, you will pick a company whose drug fails and you will be broke. If you choose, say, 10 companies like that rather than just one, you are likely to get between four and six winners and do a lot better. Biotechnology stocks are where your portfolio can really gain some alpha.

- Do your due diligence.

Check out the chairperson, the CEO and other key employees. Do they look like they belong in those jobs? Compare them to the executives you see in similar US companies.

This oldie but goodie, if a story sounds too good to be true, it almost certainly is. There are plenty of Chairpersons and CEOs out there who don’t know much about their company’s technology but have managed to weave a good story around it. A good reality check is to remember that Berkshire Hathaway, widely regarded as the most astute investment fund in the world, has achieved average an annual return of 20% since 1965 [2] , and how much is the CEO of the biopharma you are looking at suggesting it will return?

Has the technology the company is developing come from overseas? If so, further investigation is required. Good projects, like those licensed by Kazia, can be found overseas. Unfortunately, there are less scrupulous individuals around who license inevitably poor and consequently cheap technology from overseas, simply because they believe they can sell it to retail shareholders here. Some people doing this have made millions, while retail shareholders have lost as much. If a technology is being brought from overseas to list on the ASX, you need to ask yourself why? If you are in any doubt as to the quality of the technology, don’t invest.

Have quick look through the literature via www.pubmed.com and look for reviews on the technology the company you are looking at investing in is developing. You do not need to be a scientist to get a feeling for how far progressed a technology is and how much promise it has, although you need to remember that academics often have a positive bias on their own work as well. We once found a company that was studying a compound that had shown no evidence of efficacy in 11 previous clinical trials just by scanning a review.

Be very wary of topical (‘sexy’) science and the disease of the day companies. Many companies will attempt to develop a product based on a technology simply because the technology topical. For example, immunotherapies are very topical at the moment and many CEOs have been bending logic to come up with a hypothesis about how their drug could improve the performance of Immunotherapies. COVID-19 is another and probably biggest example of this. All of a sudden every ASX listed company had a compound with potential to treat COVID-19. Mesoblast was the only company with any independent verification that their cellular therapy might work.

An unapproved drug with a trade name is no better than a drug that only has an International Nonproprietary Name (INN) given to it by the World Health Organisation. INNs are effectively a generic name for the drug so that there is no confusion as to exact the chemical structure of the drug is being discussed. Moreover, a drug with an INN is no better than a drug that is simply known by a company identifier, like ATL1102. The World Health Organisation (WHO) which oversees the INN program suggests that a drug progress up to phase II trialling before an application is made for an INN

When To Enter the Market

A couple more Warren Buffett quotes seems appropriate here. The first one is “the best chance to deploy capital is when things are going down”, while the second one regarding crashes is “It’s been an ideal period for investors: A climate of fear is their best friend. Those who invest only when commentators are upbeat end up paying a heavy price for meaningless reassurance.” The point of this quote being that if you want to buy stocks that are truly undervalued your best chance to find those stocks is after events like the GFC or in biotechnology after the recent falls in products such as the IBX and IBB iShares ETFs. The reason is that investors tend to work in a sell first, ask questions later fashion when these types of events happen, such that good companies get sold down along with the overvalued companies that caused the correction or crash in the first place. Buying into stocks that are consistently being positively talked about usually means you are buying a stock in which most, if not all, of the capital gains have already been had.

The volatility of biotechnology stocks also creates buying opportunities, as the market can often discount a company or fund heavily on pure speculation, rather than common sense. The declines in the IBX and IBB seen in 2015/2016 were largely due to two tweets by Hillary Clinton in the lead up to the 2016 election regarding price gouging in the pharmaceutical industry. One was about a company called Turing Pharmaceuticals which bought a drug called Daraprim (pyrimethamine) used to treat toxoplasmosis and subsequently raised the price from USD13.50 a tablet to USD750 a tablet. The IBB closed down 5% after that tweet. In the second tweet she took aim at the price of EpiPens, used for the treatment of anaphylaxis, which had risen from USD100 per pen in 2009 to USD600 in 2016. After that tweet a range of US and overseas based companies were sold down, with Mylan, who markets EpiPen, down 5.4%. The issue here is two-fold. First-off, pharmaceutical companies rarely, if ever, receive anywhere near list price for their products. Several companies produce transparency reports each year, which detail the difference in between the list price of their drugs and the price they are actually obtaining [3]. For example, in 2020, Eli Lilly & Co only received 40% of the list price of their drugs as actual cash revenue, for Sanofi it was 46%, while for Janssen it was 47%, among other companies. The second is that the cost of pharmaceuticals in the US has been a bone of contention for as long as we can remember and a couple of tweets from a presidential candidate is a long, long, long way from actual action on drug pricing. It was highly predictable that ultimately these tweets would prove inconsequential.

The volatility of these companies also tends to attract short term traders, who, en masse, can result in a stock being drastically overvalued or undervalued quite quickly. Those quick off the mark can often grab some deeply discounted stock from traders.

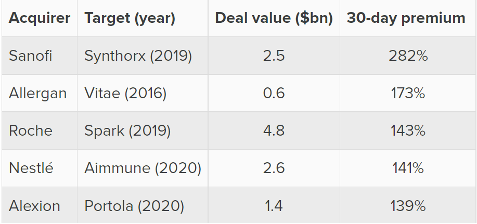

Source: Brown & Elmhirst, Evaluate Vantage Article, 19 October 2020

Trying to pick the bottom of a stock or a market is just like trying to pick the top. It is almost always due to pure luck. There is, however, nothing wrong with having a thesis which guides your time to buy. The thesis should be loose, though, because it will almost never be overly accurate.

Our thesis for a turnaround in the biotechnology sector is one based on M&A activity as measured both by deal size and number. One large deal can skew total deal value fairly easily, as AstraZeneca’s acquisition of Alexion did in 2020. When deal number goes up as well as deal value, then it becomes a safer bet that the larger biopharmaceutical companies are seeing real value across the board and that many companies may be undervalued.

Many of the compounds spun-out or sold by the larger companies during the restructuring period that haven’t failed key trials should be starting to reach a stage of development where they will become attractive to the larger biopharmaceutical companies at the right price and under their more stringent rules for progressing drug candidates, which, of course will also apply drug candidates/companies they are looking to acquire.

The acquisition premiums paid by large biopharmaceutical companies for smaller ones makes it one of the few industries where acquisition theses represent a major reason to invest. The mean acquisition premium paid in 2018 in deals worth more than USD500M based on the target’s 30 day average share price was 77.2%, in 2019 it was 102.6% and in 2020 it was 79.3% [4]. Sanofi’s bid for Principia leaked 30 days prior to the deal being officially announced in 2020 causing Principia’s stock to rise by more than 50%. Had that not happened, the mean deal value in 2020 would also have been over 100%. Exhibit 6 details the largest the largest premiums paid in deals from 2015 to late 2020. Just for interest’s sake, the highest premium paid in any deal since 2015 was Allergan’s USD1.7B bid for Tobira Therapeutics, representing a 1,532% premium to Tobira’s prior 30-day average share price, although it should be noted that Evaluate Vantage has excluded this deal as an outlier for some unknown reason.

Acquiring stock after an event, however, may be a risky move if others are of the same opinion and the price or prices spike. As such, a dollar-cost averaging approach may be a more prudent method of taking a stake in a company or fund. Yes, you may pay a bit extra, but you will certainly be there when things start to really move.

Conclusion

The declines in the IBX, IBB and locally listed ASX biopharma stocks will have shaken many investors, with the greatest effect on those investors who are not natural biopharma investors. The involvement of those types of investors in the sector, however, is a sign that the sector has over-heated. The positive signal comes when the specialist investors begin to move back into the sector. Predicting when that will occur is akin to pick the top or bottom of the stock market. Still, we believe it is likely to be M&A led and given its makeup of smaller companies, in terms of ETFs, the IBX may be the out-performer this time around. Regardless, if an investor is to take a long-term view, they will almost certainly do well as long as they enter the market cautiously, over time and, perhaps, incorporate a bit more diversification in the section of their portfolio dedicated to biopharma than they might to other sections of their portfolio.

For those investors who prefer to choose the companies they invest in and like to stay local (i.e., ASX listed), we believe Antisense Therapeutics and Kazia Therapeutics are two companies that investors can start to build their portfolios around.

THE FULL REPORT CAN BE DOWNLOADED FROM EITHER THE ANTISENSE THERAPEUTICS OR KAZIA THERAPEUTICS COMPANY PAGES.

ENDPOINTS

[1] Dowden & Munro (2019) Nat Rev Drug Discov

[2] Sean Williams, Motley Fool Article, 13 October 2021

[3] Adam Fein, Drug Channels Article, 14 April 2021

[4] Brown & Elmhirst, Evaluate Vantage Article, 19 October 2020