by Pieran Maru – Investment Analyst

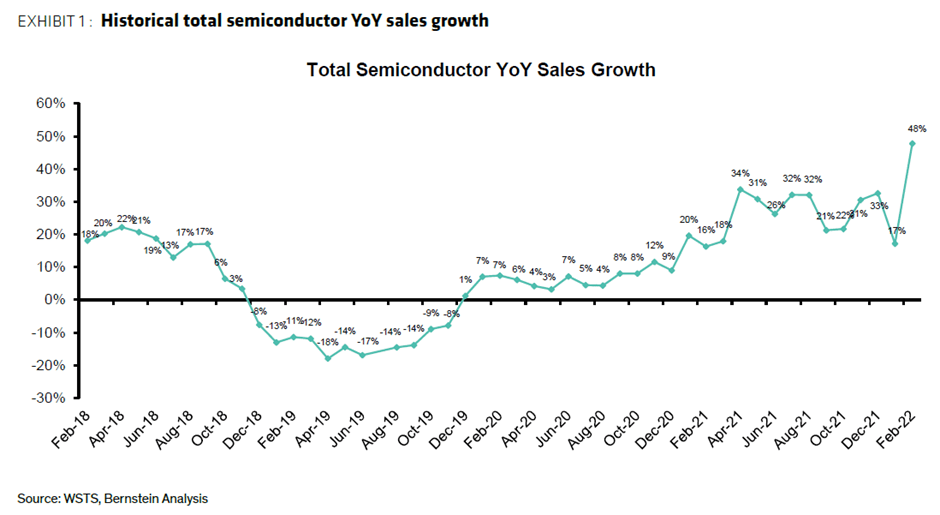

What initially caused the shortage of semiconductors? A classic mismatch of demand/supply on the semiconductor cycle, with a pandemic catalyst. In the lead up to 2020, we saw rising tensions between the US and China, as several Chinese companies were added to the US Entity List.

By March 2020, unexpected demand entered the cycle with increased consumer electronics orders, as firms adjusted to remote working. Demand was also supported by increasing inventory build up due to continued geopolitical risks while unpredictable rolling outages due to lockdowns further tightened the supply end. Recent estimates place the cost of China’s zero-Covid policy at approximately USD 46 billion a month (3.1% of GDP) while Brian Deese, director of the US National Economic Council, estimates the semiconductor shortage “probably took a full percentage point off of GDP in 2021.” (estimates as at 31 March 2022).

Automotive

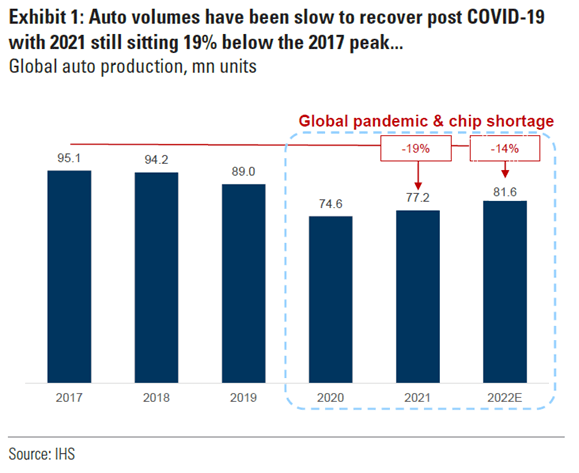

One industry heavily impacted by the supply constraints is automotive. Mercedes sales fell 15% in Q1, with Ford’s total sales dropping by 25.6% compared to the year prior. We can see this imbalance having knock on effects in the second-hand car market with a number of cars now selling at a premium to list. Semiconductors are essential to the production of modern day cars – from advanced driver-assistance systems to braking systems. Without them, production can soon come to a halt. Recent examples this quarter include the Mini plant closing for two weeks due to shortages while Tesla’s factory in Shanghai closed temporarily during a local lockdown and to abide by community orders.

Neon Gas

Neon is an essential noble gas used for excimer lasers as part of the lithography process in the production of semiconductors. Neon makes up ~0.0018% of air and is isolated as a byproduct, predominately by the steel industry using an Air Separation Unit (ASU). There are approximately 28 large ASUs globally with ~10 locations around the globe able to purify the crude mixture. With two of the leading suppliers of neon based in Ukraine having stopped production, estimates place the impact on world supplies at 30%1. At present, this is not expected to impact the semiconductor shortage materially further, in our view, given companies have built up strategic inventories with a number of global suppliers and have been able to further diversify sourcing since 2014. With the significant rise in neon prices, we expect more ASUs to be built and expect normalisation to occur by the end of the year.

Equilibrium in sight?

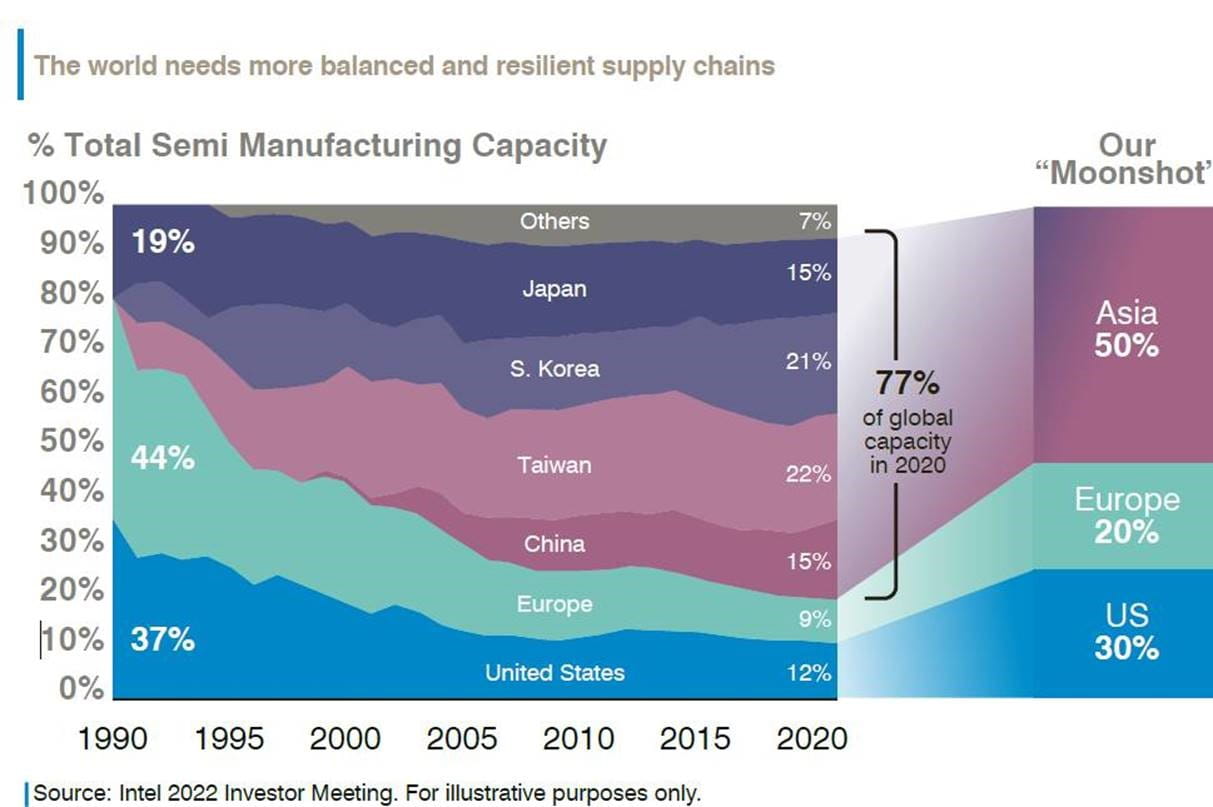

The US Senate recently approved an amended bill to provide USD 52 billion for the US semiconductor chips – now currently sitting at the ‘resolving differences’ stage of the legislation process. This would allow manufacturers to reduce reliance on supply chains from other countries and support domestic semiconductor production, research and development. While from a European perspective, the European Commission announced a framework of measures for strengthening their semiconductor ecosystem, which will add EUR 15 billion to an existing EUR 30 billion already planned. President von der Leyen highlighted two main goals in her statement on 8 February: First, to increase resilience to future crises and second, to make Europe a leader, with the aim of representing 20% of global market chips production by 2030 (currently 9%). This would imply an estimated fourfold increase in effort, given demand is expected to double by then. The current heavy reliance on Asia for semiconductor manufacturing can be seen from Intel’s 2022 Investor meeting (figure below), highlighting the shift in geographical location over time and in their view, the expected “moonshot” distribution in the future.

The global supply constraints have highlighted how critical semiconductors are in all industries and the importance of maintaining a level of inventory to ensure minimum disruption. This has caused companies to move from a “just in time” inventory to “just in case” elevated levels. However, it remains to be seen if or when the impact of excess and duplicate ordering will begin to show as orders are filled and customers stop building inventory.

Click here to view the Disruptive Strategist newsletter in full.