The Axis is tilting dangerously – to re-balance, the free-World’s energy investment must rise

Russia’s violent invasion has tragic consequences for the peoples of the Ukraine. It has also galvanised to action a coalition of nations and reenforced an existing geopolitical trend. This is for many nations to seek to reduce trade reliance upon the so-called Axis of Authoritarian countries.

Trade is built upon trust – but this has been soured by economic coercion, debt-bondage of Developing Nations and militarisation of disputed territories. Now, by outright invasion.

Oil, gas and coal prices have been rising for over a year before the invasion of Ukraine. The invasion’s impact on fuels prices has turned discomfort to outright pain for many consumers. Energy markets are delivering a strong message.

What’s needed – The World needs to commence a period of re-investing in oil & gas and nuclear energy supply chains. This is to mitigate past under-investment and to mend the medium-term impact of the Ukrainian War. This investment would complement and assist making the energy transition to renewables more affordable.

While energy prices are volatile, they likely to remain at elevated levels so for as long as there is the imperative to wean the World off Russian energy. Europe is starting to get the message, but are we?

We have achieved this before – The oil shocks of the 1970’s led to a transformation of the way oil and energy was sourced, used and priced by the mid-1980’s. The task of reducing Russia’s energy coercion today is less than diminishing OPEC’s market power in the 1980’s.

Russian oil and gas exports matter – but the solution is in investors’ hands

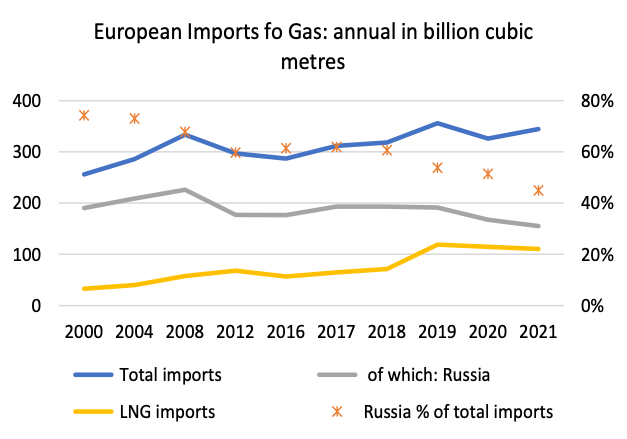

Russia’s ability to coerce other nations can be reduced by minimising dependence upon its critical energy industries. Russia produces ~11.3 million bbl/day or 11% of the World’s total oil output and exports 7.6 mb/d of crude and products, or a bit over 8% of the World (excluding Russia’s oil consumption). Russian piped gas exports to Europe comprise around half of its imports of natural gas and its LNG helps power Japan and some other countries. These are daunting dependency levels for Europe and the World to eliminate.

Can we achieve an increase in energy output to radically reduce the dependence upon Russia?

Russia’s oil exports are sizable – but with investment are replaceable

Reducing Europe’s dependence on Russian gas – is a trend that needs to accelerate to reduce its coercive influence

The solution to ultra-high prices and coercion, is high-ish prices and concerted investment

The current high prices for oil, gas, coal and uranium are signals to reverse a multi-year and general neglect of investment across the broader resources industry over the last decade. This is needed merely to maintain current levels of energy consumption.

The added need to re-tool the global economy for the energy transition increases use of the traditional energy and minerals, think nickel and steel, plus materials like concrete that need energy inputs to, in turn make wind and solar facilities and the required transmission lines. Lithium-Ion battery input costs have soared over 80% in 15-months, due to demand outstripping materials supply.

We need to invest in both green energy and at least some replacement investment in gas and oil; and to expand mined uranium and its processing facilities.

The geo-political imperative to reduce a military aggressor’s export funding is just an additional layer of resources supply shortfall. High prices do ration use and can slow consumption and economic growth. However, this pain is for naught, if the signal to raise capacity is ignored by the investment funds and banks due to their well-meaning energy transition policies.

Active energy investment in supply and it’s use – has worked before in the 1980’s

We believe that well-directed energy investment in renewables, uranium and oil & gas fuels can transform the current chaos into steady growth and shut-in Russia in the meantime. That is until Russia changes its aggressive ways and can be welcomed back to the ranks of free trading nations.

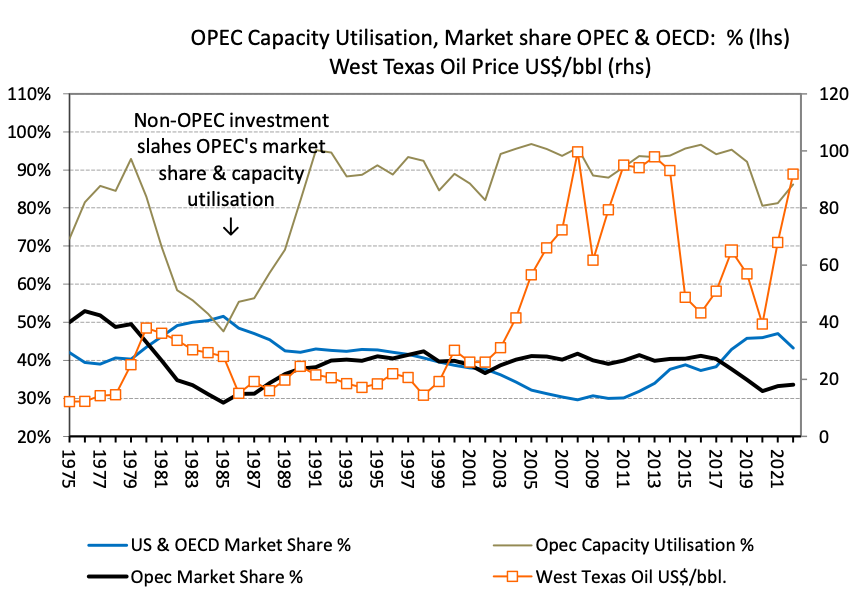

The OPEC-inspired oil price shocks in the 1970’s catapulted oil prices from below US$2//bbl to ~US$38/bbl because a radicalised OPEC controlled more than half the global oil market. These shocks contributed to a major bout of stagflation, particularly as the World then relied more heavily upon oil than it does today.

However, the oil price rise unleashed massive rotation in the patterns of consumption of oil. Fuel oil for power was swapped for coal, gas and uranium fuelled electricity generation. Fuel efficiency of vehicles and heating in homes and industry were dramatically improved. This transition took big investment in the 1980’s and provides us encouragement that the current required transition to renewable generation can be achieved, even without Russia’s resources.

Oil’s supply-side profile in the 1980’s was utterly transformed. High oil prices enabled risky drilling in new basins and into deeper waters like the North Sea, Alaska, Gulf of Mexico and saw the rise of Canadian synthetic oils.

Amazingly the OECD members’ oil market share overtook OPEC’s share as OPEC grimly hung on to producer-set pricing. That is, until 1985 when OPEC controlled less than 30% the global market and its capacity utilisation fell toward 50%. OPEC lost control of pricing. See chart below.

Replacing Russia’s oil is a smaller task than the non-OPEC World faced in the 1980’s.

The World oil supply changes reshuffled a massive ~20% of oil market share in the 1980’s. This delivered better energy market outcomes. The current oil challenge of shutting-in Russia amounts to around 8% of global import needs. The need to replace Russian gas is a further challenge, however the increasing number of LNG exporting nations makes this goal more achievable. We note that the Japanese Government announced they would assist Japanese companies to invest in accelerating LNG expansions.

The task is also lightened as the World has better technological and renewable solutions to diversify energy use away from oil and ultimately also gas. The emergence of safer, more modular, and cheaper nuclear reactors also has a transformative role in the 2030’s. The time to add greenfield sources of uranium (and its enrichment processes) away from Axis coercion, is now.

Importantly, from a carbon-balance perspective, Russia’s lost fossil fuels sales in the coming decade, may never be produced as the world’s energy demand patterns would have moved on.

Perhaps controversially this analyst’s observation is that OPEC’s role in markets has been (mostly) positive since the early 1990’s. It also has sought to meet global market’s needs to stop unwarranted price rises. This contributed to an overall force for market stability and sensible policy born from its hard-won experience. Its policies regained and largely sustained a reasonable market share of 35% to 40% for OPEC for nearly 30-years.

A proactive investment stance to replace Russian fossil fuel imports with a mix of renewable energy, uranium, oil and gas production will in time alleviate energy price pain. Like OPEC, it may even result in Russia changing its policies, for the better.

To rectify today’s energy supply chain weaknesses and reduce national security vulnerabilities – the message is clear…

Invest in renewable energy, oil, gas and uranium and in energy consumption efficiencies

Debt providers and equity investors should support sensible investments in both the energy supply and also the energy consumption efficiency sides of the market. This is to gradually reduce the impact of past under-investment and increase the free World’s resiliency to the shocks of the increasingly belligerent Axis group. This is self-help that promotes sustainability.

However, the recent oil & gas price windfalls are not yet translating to a massive re-investment program. Recently ExxonMobil tripled its share- buyback program to US$30 billion and Chevron said it will repurchase a record $10 billion of stock this year. Santos also recently introduced a US$0.25 billion buyback.

The reticence of Major oil & gas companies to invest is an opportunity for more nimble companies and their shareholders to reap investment rewards for delivering capacity the global market and our collective security-needs demand.

Investment in energy supply side should include both capacity replacement in fossil fuels and uranium for this decade to provide lower cost inputs for the accelerating expansion of renewable power and batteries we need for the 21st Century transition.