by Tal Lomnitzer, Portfolio Manager – Global Natural Resources

Key takeaways

- The team’s analysis suggests that resources equities have shown a negative correlation with the broader equity market over the long term, yet are capable of generating similar returns with lower volatility.

- In an environment of rising inflation, certain sectors such as mining, packaging and forestry can have a good correlation with inflation expectations and are beneficiaries of decarbonisation.

- The prospects for resources companies are bright. Sustainable natural resource companies have a key role to play in supporting the transition to a more sustainable and low-carbon economy.

Note: this article was first published in October 2019. We have re-run the data in our analysis against the MSCI World Index to provide a more global perspective compared to the S&P 500 used previously. The key message remains – resources equities can be an effective portfolio diversifier.

Think longer term to extract the best from natural resources

The global natural resources sector is generally considered to be highly cyclical, being sensitive to the economic backdrop, resulting in a strong temptation among investors to time their entry and exit with the economic cycle. We sympathise. Getting the timing wrong can be a career-limiting decision while getting it right can be extremely rewarding so it is natural to be captivated by the short cycle outlook. A myopic focus can however, miss the significant benefits of taking a longer-term perspective.

We encourage investors to consider an investment in the resources sector over the long term ‒ to think of resources as an investment rather than a trade. Unlike other segments of the market, resources equities (i.e. materials, energy and agriculture) have shown they can be negatively correlated with the broader equity market over the long term. Yet they are capable of generating similar returns.

Similar return with lower risk is considered by some to be a holy grail of investing ‒ resources, anyone?

Essential building blocks

Resources provide the essential and fundamental building blocks of economic development. While demand for some commodities like coal or oil is likely to plateau and decline, the demand for others is growing and looks set to rise. The renewable energy industry requires copper, lithium, cobalt, nickel, iron ore and silver. Digitisation requires massive server farms and enormous quantities of energy. As the world strives towards a digitised, electrified and fossil fuel-free future, resources have an integral and essential part to play. There is a fundamental growing demand for future energy sources and nutrition ‒ that can only be met by the resources sector. As the world evolves so does the need for different parts of the resources sector.

Benefiting from negative correlation over time

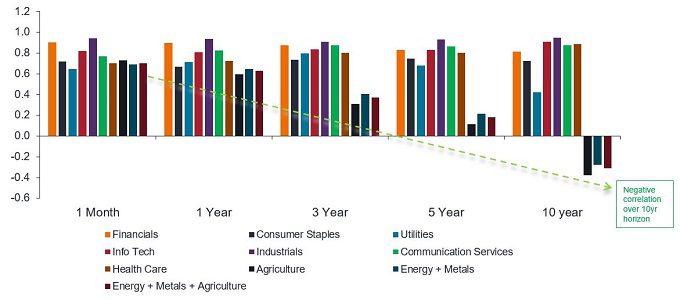

A 2016 white paper by Lucas White and Jeremy Grantham at GMO*, showed that “resource equities provide diversification relative to the broad equity market, and the diversification benefits increase over longer time horizons”. We set out to test this hypothesis on a broader data set that includes agriculture. Building on from their analysis, we disaggregated the US market into its various sectors and ran correlations between the sectors and the MSCI World Index (the market) over various rolling time periods using data from February 1995 to February 2022 (see chart 1).

We defined resources as an equally-weighted index of mining, energy and agriculture, broadly similar to the S&P Global Natural Resources Index. The analysis shows that the linkage between resources equities, other sectors and the market is high over the short term but declines dramatically over the longer term. Indeed, over a rolling ten-year period the correlation between resources and the broad market has actually been negative whereas it stays positive and rises over time for other sectors.

*GMO white paper: An investment only a mother could love: the case for natural resource equities, Lucas White and Jeremy Grantham, September 2016.

Chart 1: Resources equities have been negatively correlated with broader equities over the longer term

Source: Bloomberg, FactSet, Janus Henderson Investors. Correlation of resources (energy + mining + agriculture) to other MSCI World Index sectors, monthly observations from February 1995 to February 2022. Past performance does not predict future returns.

Potentially higher reward for less risk?

Beyond the ongoing contribution to wealth creation and quality of life, resources have the attributes of an attractive investment class in their own right. As with gravity in the domain of physics, there are certain immutable laws of investment, in particular, the relationship between risk and reward. Our analysis suggests that by adding resources to an equities portfolio it is possible to generate a similar return but with lower risk as measured by volatility (standard deviation).

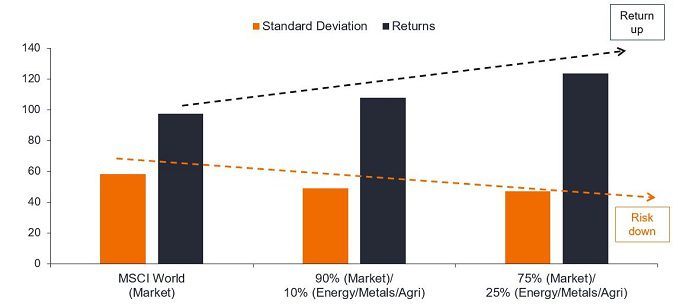

Taking inspiration from GMO’s whitepaper, our analysis of more than 25 years of historical data shows that when compared against the market, the average ten-year return of a portfolio consisting of 75% MSCI World Index and 25% resources has increased while the standard deviation (the risk) has dropped. Interestingly, the results are consistent though less dramatic if a 90% MSCI World/10% resources portfolio is used (see chart 2). Unsurprisingly, combining these metrics into a Sharpe ratio shows a similar result.

Chart 2: An allocation to resources may improve risk-adjusted returns over the long term (10 years)

Source: Janus Henderson Investors and Factset. Rolling 10-yr standard deviation and returns based on hypothetical portfolio allocations to the MSCI World Index and resources equities (energy + mining + agriculture). Monthly observations from Feb 1995 to Feb 2022. Hypothetical examples are for illustrative purposes only and do not represent the returns of any particular investment. Past performance does not predict future returns.

Schrödinger’s cat

Quantum physics teaches that something can exist in two states. Matter is both a particle and wave; resources equities are both cyclical and an effective portfolio diversifier. In Schrödinger’s words “this would not embody anything unclear or contradictory”. The answer lies in the timeframe. While resources are tied to the economic cycle in the near term, over longer time periods they tend to march to the beat of their own drum. Not everyone thinks in ten-year horizons, so we have re-run the risk/return analysis over rolling five-year periods using the same data and generated similar results.

To summarise, over five or ten-year horizons, adding resources including agriculture, as a core part of a portfolio is likely to engender better returns with lower risk. Instead of looking on the sidewalk for pennies it is far better to look to the horizon for nuggets of gold.

Furthermore, in an environment of rising inflation an investment in the resources sector has additional attractions. Mining equities have been shown to have a good correlation (positive relationship) with inflation expectations and can be considered to be a real asset play as we move into negative real rates. The sector is not being technically disrupted, in fact, it benefits from the disruption within the energy and mobility sectors: renewables use much more copper or steel than fossil fuels, while electric vehicles require much more copper than combustion engines.

Similarly, packaging and forestry have a high correlation with inflation expectations and are benefiting from a move to ecommerce and the replacement of plastics with fibre-based packaging. There are many companies in the resources sector that appear well positioned compared to the rest of the market in terms of balance sheet strength, cashflow generation and dividends. The team believes current valuations appear attractive and a long term-investment could well be rewarding.

Resources play a key role towards sustainability

We are optimistic about the prospects for natural resources companies, which are at the nexus of sustainable development and the decarbonisation transition. While some resource sectors have potentially high environmental and social impacts associated with their extraction, production, manufacture, and distribution, we believe that sustainable natural resource companies have a key role to play in supporting the transition to a more sustainable and low-carbon economy. In our view, companies that adhere to sustainable practices are best prepared for the future and are therefore more likely to deliver attractive, risk-adjusted returns.