Introduction

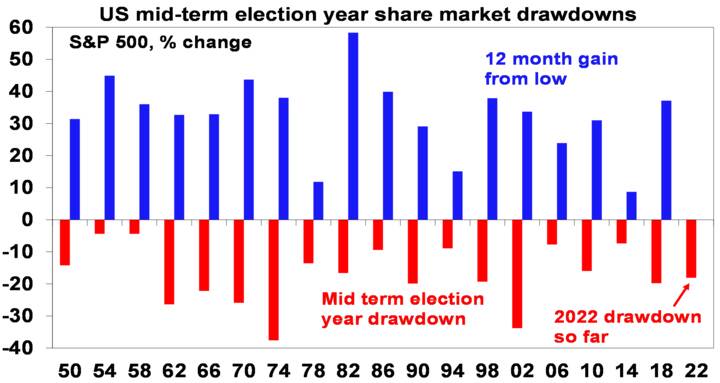

Last year saw very strong investment returns and was relatively calm in investment markets. While there was a lot to worry about, the biggest drawdown in US shares was 5% and in Australian shares it was 6%. This always seemed unlikely to be repeated and it certainly hasn’t been so far in 2022! While they have had a good bounce from last week’s lows, from their cyclical highs US shares have had a fall of 18% to their recent low, global shares have had a fall of 17% and Australian shares have had a fall of 9%. This has been led by tech stocks with Nasdaq having had a plunge of 29%. Mid-term election years in the US are known for below average returns and a rough ride with an average top to bottom drawdown of 17% and this has already been surpassed.

Source: Strategas, AMP

At the same time government bonds are having worse losses than in the bond crash of 1994 (don’t forget that when bond yields rise their capital value goes down) and crypto currencies have also been hit hard with 50% plus falls in prices.

So where are we?

What’s driving the volatility – the big negatives

The plunge in share markets reflects a combination of factors.

- Shares were vulnerable to a rougher ride this year. After strong gains from pandemic lows shares were no longer dirt cheap. Speculative froth was evident in tech stocks, meme stocks, SPACs and cryptos. Relatively calm years like 2021 are often followed by a rough year.

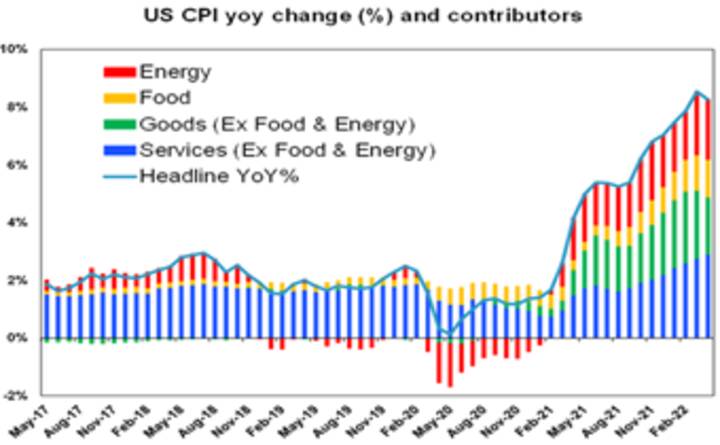

- Inflation continues to come in stronger than expected largely due to pandemic related supply disruptions and strong goods demand, but also labour shortages and “reopening” impacting wages and hence services prices. While US annual inflation fell slightly in April (from 8.5%yoy to 8.3%) as higher monthly inflation readings a year ago dropped out it was still higher than expected. Goods inflation (green bars in the next chart) looks to be slowing but services inflation (blue bars) is continuing to pick up partly reflecting the surge in wages growth seen recently in the US. So while inflation may have peaked it looks like staying too high for comfort for the Fed (and other central banks) for a while yet.

Source: Bloomberg, AMP

- Rising pressure for wage growth to compensate for inflation risks resulting in a wage/price spiral and a rise in inflation expectations that locks inflation in at high levels. Talk of 5% wage claims in Australia suggests this is also a risk locally.

- The war in Ukraine has added to supply constraints in relation to commodities. Fear of an escalation resulting in a cut to Russian gas to Europe &/or including NATO countries in direct fighting have added to market jitters with Finland & Sweden wanting to join NATO further annoying Russia.

- The war in Ukraine has further boosted geopolitical tensions which does not go down well with share markets.

- Lockdowns in China under its zero Covid policy in response to Omicron outbreaks have hit Chinese growth and further disrupted global supply chains. This has seen a sharp fall in Chinese economic data for April with industrial production down 2.9% on a year ago and retail sales down 11.1%.

- The surge in inflation has seen central banks step up monetary tightening. Even the ECB looks like it might start hiking rates in July. While the rise in inflation is mainly driven by supply, demand has been strong too and central banks have to act to stop high inflation boosting inflation expectations which will lock inflation in at high levels.

- The longer inflation stays high the more investment markets worry that central banks will not be able to tame it without bringing on recession. As Fed Chair Powell indicated, getting inflation to 2% will “include some pain”.

- And as bond yields rise in response to higher inflation this puts further pressure on share markets by making them look relatively less attractive to investors.

- Just as tech stocks and particularly crypto currencies were the biggest beneficiaries of easy money and low rates, they are the biggest losers of monetary tightening. With the end result that cryptos are moving like a high beta version of shares (and so are no portfolio diversifier) and have offered no hedge against the rise in inflation over the last year.

After plunging into last week, shares could have a further near-term bounce. But risks around inflation, monetary tightening, the war in Ukraine and Chinese growth remain high and still point to more downside in share markets. While investor pessimism is extreme (positive from a contrarian perspective), we have not yet seen levels for indicators like VIX or the ratio of Put options to Call options seen at major market bottoms.

It’s not all doom and gloom

However, there is some light at the end of the tunnel.

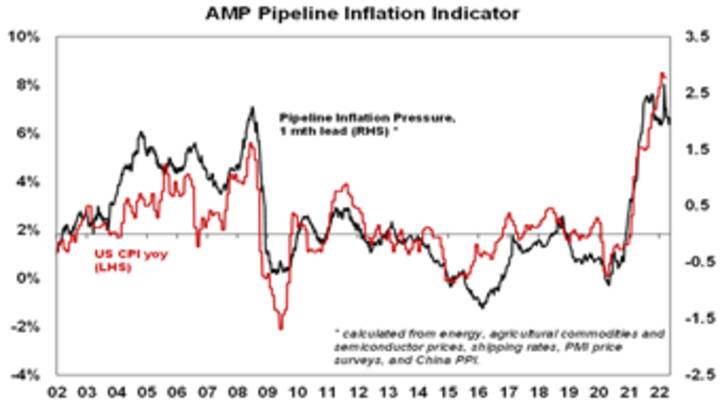

- While US inflation is still too high for comfort and may remain so for a while, signs of some peaking are evident in our Pipeline Inflation Indicator reflecting lower freight costs and a slowing in commodity prices. This could enable central banks to slow the pace of tightening later this year or early next in time to avoid recession.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Macrobond, AMP

- While services inflation could continue to rise for a while yet there are signs US wages growth may have peaked with eg monthly growth in average hourly earnings looking like it may have peaked late last year.

- Share market earnings are continuing to come in stronger than expected. US March quarter earnings reports continued to surprise on the upside and earnings look on track to rise around 12%yoy which is up from initial expectations for a 4.3%yoy gain. And earnings growth in Europe and Asia is averaging slightly faster.

- Some of the risks around a widening in the Ukraine conflict may be declining. Contrary to the fears of many, President Putin did not declare war on Ukraine and announce a general mobilisation signalling an escalation at his 9 May victory over Nazi Germany commemoration speech. It could become another frozen conflict which is horrible for Ukraine but not a further disruptor to global growth.

- Covid cases in China appear to be slowing which could enable an easing in restrictions and clear the way for policy stimulus to boost growth.

- Yield curves or the gap between long-term bond yields and short-term rates have yet to decisively invert (or warn of recession) and even if they do now the average lead to recession is 18 months – which takes us to late next year which would be too early for share markets to discount as they only look 6 months ahead.

- Just focussing on rate hikes ignores the tightening already underway from the ending of money printing, meaning that the Fed may have already tightened a lot and market expectations for a cash rate up to 3% in the US (and Australia) next year may be too hawkish.

So while shares could still see more falls in the short-term we remain of the view that a deep (or grizzly) bear market will be avoided as US and Australian recession should be avoided over the next 18 months, which should enable share markets to be up on a 12 month horizon.

Could a crypto currency meltdown de-rail things?

Now that easy money is being reversed crypto currencies are suffering along with tech stocks. The risks were highlighted in the past week with the collapse of TerraUSD, an algorithmic stablecoin meant to stay at $US1, with a flow on to demand for other cryptos, including Bitcoin. Notwithstanding short-term bounces, further downside is a risk if falls feed on themselves and the speculative mania in crypto unwinds, leading to yet another 80% top to bottom fall. And to the extent crypto currencies depend on bringing in more investors to keep moving forward, a collapse now could have a more lasting impact on interest in it than in the past when it was less “mainstream.” Particularly given that Bitcoin has so far offered little hedge against inflation over the last year. For the broader financial system and economy, a crypto crash poses a risk but it’s unlikely to be another sub-prime/2008 US housing crisis. Banking system exposure to crypto is limited and the exposure of the wider public is still small (unlike it was to US housing).

What about Australian shares?

Australian shares are vulnerable to further falls in the short-term along with global shares. However, as noted earlier they have been relative outperformers through the decline in share markets so far and this is also evident year to date where global shares are down 13% and Australian shares are down 4%. This reflects their exposure to strong commodity prices and low exposure to tech stocks. While Chinese Covid lockdowns may weigh in the short-term, Australian shares are likely to continue to outperform over the medium-term as the commodity super cycle continues – on the back of constrained supply reflecting low levels of resource investment, decarbonisation and geopolitical tensions – and as higher bond yields compared to the pre-covid era weigh on tech stocks.

Key things for investors to bear in mind

Sharp share market falls are stressful for investors as no one likes to see their investments fall in value. But at times like these key things for investors to bear in mind are that: share market pullbacks are healthy and normal; in the absence of a recession share market falls may be limited; it’s very hard to time market moves and selling shares after a fall locks in a loss; share pullbacks provide opportunities for investors to buy them more cheaply; Australian shares still offer an attractive income flow relative to bank deposits; and finally, to avoid getting thrown off a long-term investment strategy it’s best to turn down the noise around all the negative news flow.