by James T. Tierney jr and Michael Walker

For several years, the largest US technology and new media companies were widely seen a cluster of similar stocks. Not anymore. The recent divergence of the so-called FAANGs reminds us why fundamentals should always trump fads for long-term equity investors.

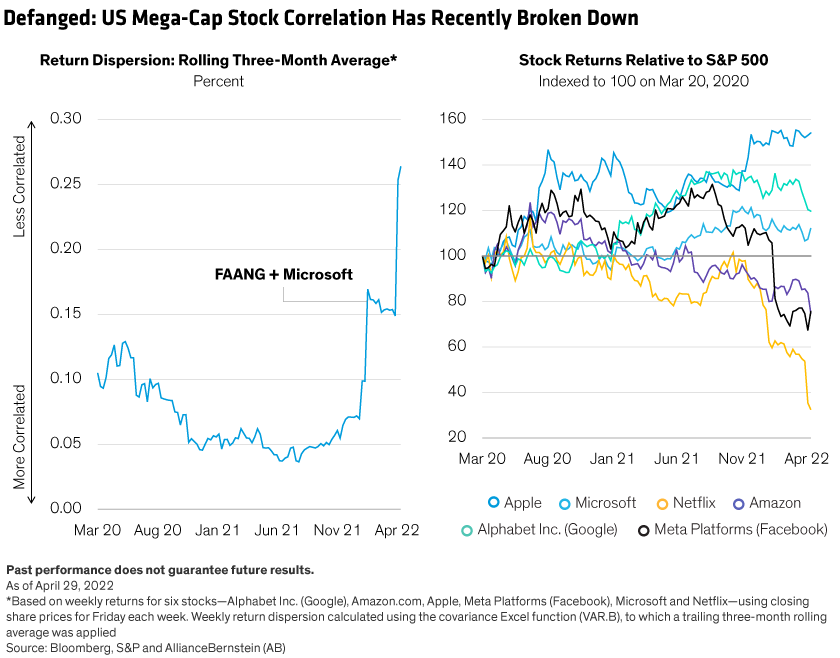

It’s one of the most widely known acronyms on Wall Street in recent years, even as it became clumsier to pronounce. First came the FANGs—Facebook (now Meta Platforms), Amazon, Netflix and Google. Apple later joined to create the FAANGs, and more recently, a revitalized Microsoft came aboard to the FAANMGs. The acronym reflected a popular view that these stocks were made from the same mold. And their performance was highly correlated, especially during the pandemic, when demand for digital services surged. As a result, these six stocks comprised nearly 39% of the Russell 1000 Growth Index, and 24% of the S&P 500 at the end of 2021.

Market Correction Amplifies Differences

Much has changed during this year’s correction. While all six stocks have declined, Netflix and Meta fell harder than the others. The correlation has faded, and returns have diverged (Display).

In recent years, we’ve frequently warned of concentration risk in US equity markets. When the FAANGs rose in tandem, passive investors enjoyed handsome returns but also accumulated a hefty weighting in the priciest US mega-cap names. In our view, each company should be researched and held based on its merits, using a disciplined investing approach and at measured weights.

Evaluating Strengths and Weaknesses

Even after the declines, US mega-caps are still large components of US indices, so they can’t be ignored. But an active approach is essential to find those offering profitable, sustainable growth at the right price. The technology and media industries offer an array of business opportunities from cloud computing, search engines and social media to streaming, hardware and online shopping.

Since each segment faces different dynamics and regulatory pressures, business outcomes will differ. Media streaming is seeing signs of saturation while also becoming much more competitive. Social media incumbents are fending off new competitors. Unprecedented inflationary pressure is adding hurdles to e-commerce. The cloud is being elevated by the digital transformation boom. Smartphones have become an indispensable, regularly upgraded utility.

Of course, all this was true before 2022. But now the market is making the distinction that there will be winners and losers, unlike the last five years where everyone was seen as a winner. Evaluating the fundamental strengths and weaknesses of each company is the key to investing successfully in the right mega-cap growth companies for a more challenging macroeconomic and market environment.

Michael Walker is Senior Research Analyst and Portfolio Manager for Concentrated US Growth at AllianceBernstein

James T. Tierney, Jr., is Chief Investment Officer for Concentrated US Growth at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable.