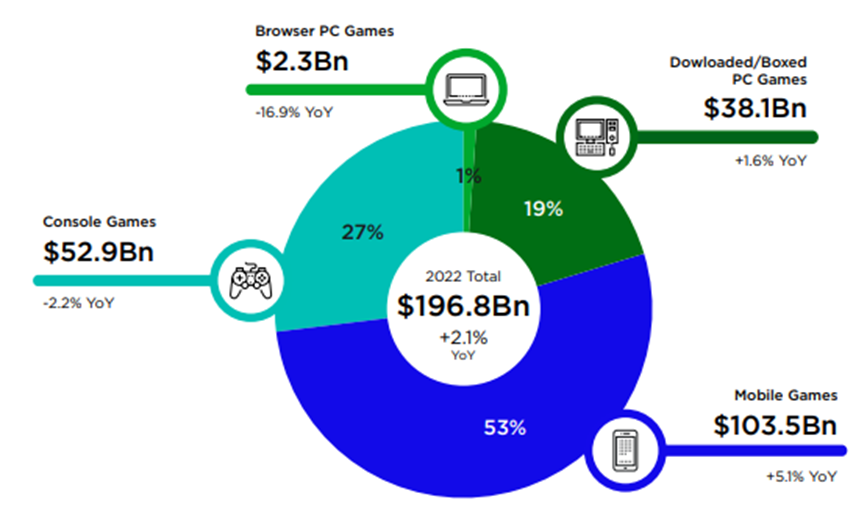

The multi-billion-dollar esports and gaming sector is among the fastest growing industries in the world. Recent forecasts by data firm Newzoo predict there will be 3.2 billion gamers worldwide in 2022, that’s over a third of the global population. The industry is expected to generate over US$196 billion this year, gaining 2.1 per cent on 2021.

Despite rapid growth during the pandemic years, the sector has slowed in recent months, with companies posting mixed second quarter results in the US. The slowdown comes as many gaming firms contend with supply chain delays, and a shift in consumer choices due to easing lockdowns.

Analysts and industry experts, however, are confident the sector will continue to grow above pre-pandemic levels, pointing to the launch of delayed titles and an easing of parts shortages as tailwinds in the short-term. “Long-term growth remains in place,” says Morningstar analyst Neil Macker.

Esports and gaming second quarter earnings round-up

Gaming company, Electronic Arts (EA) had a strong second quarter, posting a 50 per cent rise in profits, and revenue growth of 14 per cent. The business focuses on live services and sports games such as FIFA, Madden NFL, Battlefield and Apex Legends which are played on mobile devices. The stock recently received a US$155 dollar price target from Bank of America and a buy rating.

“EA is proving its mastery of monetization with record sales for FIFA Mobile for the quarter, the highest sales for the FIFA franchise, and a 40 per cent increase in daily average players. EA has managed to corner the sports video games market with FIFA, NFL Madden, and its recent addition F1” says Joost van Dreunen, a lecturer on the business of games at the NYU Stern School of Business.

EA CEO Andrew Wilson is optimistic about the company’s outlook, “As the supply chain starts to ease, our expectation is that more and more people pick up that next console.”

Meanwhile, Chipmaker Advanced Micro Devices posted beats on both top and bottom lines. Rosenblatt analyst, Han Mosesmann sees upside potential for the company, recently issuing a “buy” rating on the chipmaker along with a US$200 price target. This would infer a near-doubling of its share price.

Gaming company Take-Two also surprised to the upside. Its net revenue lifted 36 per cent to US$1.1 billion, while recurrent consumer spending increased 44 per cent. It’s the video game company with the best potential for appreciation according to Macker. “Its recently completed purchase of Zynga has transformed the firm into the traditional publisher most leveraged to mobile. The US$11.2 billion deal is the largest-ever closed video game acquisition, but we think Zynga will engender enough opportunities and benefits to justify the high price tag. One key opportunity will be developing mobile versions of Take-Two’s premier franchises, including Grand Theft Auto.”

A number of companies in the video game sector however, didn’t fare so well. Firms such as Activation Blizzard and Nintendo noted that gamers spent less money overall in the second quarter.

Rising prices and a lack of hit titles also added to problems for Activision Blizzard.

Chipmaker Nvidia released preliminary results that show second-quarter revenue of US$6.7 billion, below its initial forecast of US$8.1 billion. The company says the shortfall primarily reflected weaker-than-forecast gaming revenue.

Online game platform Roblox, results missed analyst’s estimates, but CEO Dave Baszucki told Bloomberg the company, “just had the biggest month in its history as far as engagement, as far as users in the US, in Canada and around the world, in all age demographics.”

Positive outlook for esports and gaming

Data firm New Zoo says games market revenues are still growing, despite supply chain issues, global economic challenges and the return of non-home leisure spending. Some segments of the market, however, are stronger than others.

The primary driver of revenue growth across the world’s games market is mobile, which will generate revenue of US$103.5 billion this year (53 per cent of the market), an increase of 5 per cent on last year.

Meanwhile, the personal computer market is expected to increase by 1.6 per cent to US$40.4 billion, but console games will decline 2.2 per cent to US$52.9 billion.

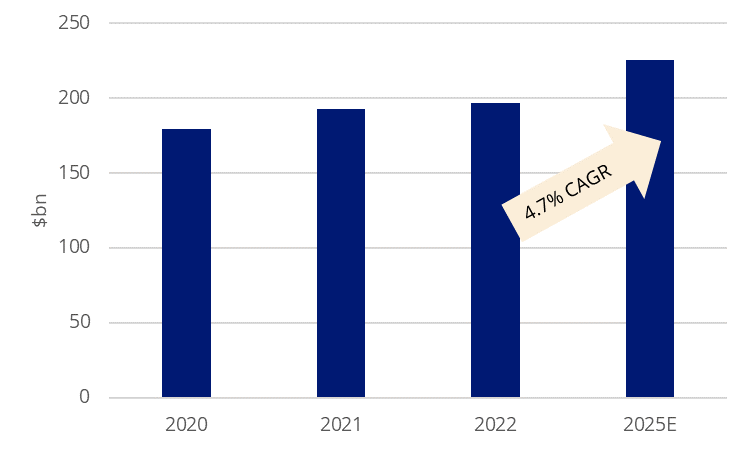

Figure 1: Global spending on gaming forecast

Source: Newzoo

Newzoo forecasts global spending on gaming will reach $225.7 billion by 2025, representing a compounded annual growth rate of 4.7 per cent between 2020 and 2025.

Figure 2: Global Game Revenue Forecast

Source: Newzoo

Streaming Platforms

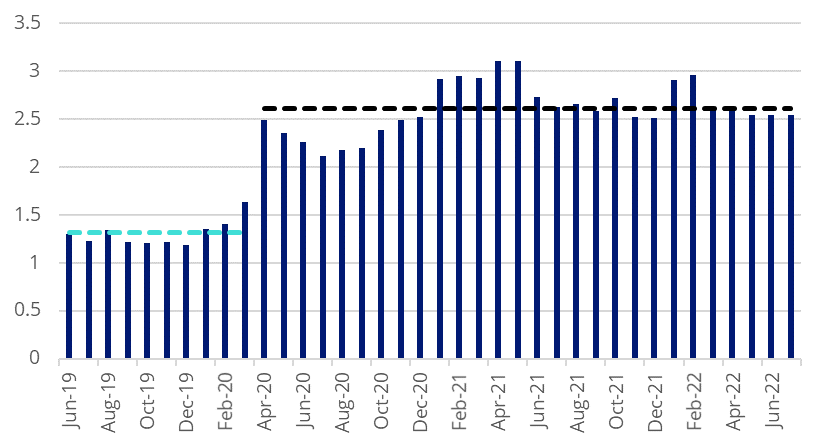

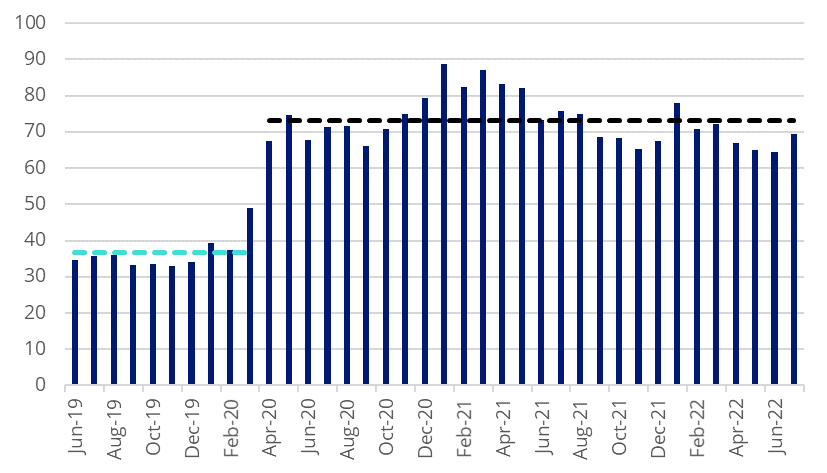

Data from streaming platforms such as Twitch, meanwhile indicates both viewers and streamed hours remain above pre-pandemic levels. The trend is reflective of the robust growth in esports, which is providing tailwinds to spending on hardware such as gaming-specific headsets, keyboards and computer chips.

Figure 3: Average Concurrent Viewers by Month (mn)

Source: TwitchTracker as of 31 July 2022

Figure 4: Total hours streamed (mn) on Twitch

Source: TwitchTracker as of 31 July 2022

Esports

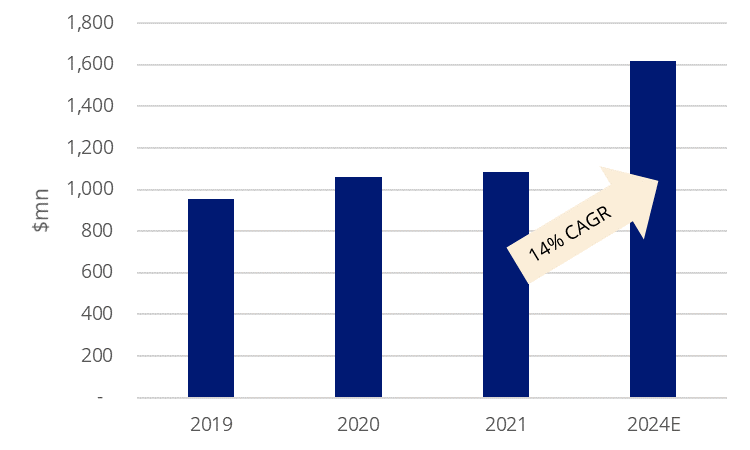

Goldman Sachs expects the global esports market to grow at a robust 14 per cent compound annual growth rate (CAGR) between 2021 and 2024 and there are signs the virtual sporting arena is becoming more mainstream. esports was included as a pilot event in the 2022 Commonwealth Games, and there are hopes it could become part of the full program by the next games in 2026.

Meanwhile, Mastercard has just signed a three year agreement with Saudi esports federation (SEF) as an official sponsor of gamers8, a gaming and esports event. Mastercard and SEF will collaborate on metaverse and augmented reality (AR) activations, non-fungible tokens (NFTs), gamers’ and fans’ loyalty solutions, and a gaming virtual MasterCard card.

Gaming and esports consumption in Saudi Arabia is expected to reach US$6.8 billion by 2030, according to a recent report by Boston Consulting Group.

The increasing mobile usage in emerging countries, rising awareness regarding esports, and increasing popularity of video games are expected to fuel the market growth over the next decade.

Figure 5: Esports Revenue 2019-2024E

Source: Goldman Sachs, Logitech

Global growth

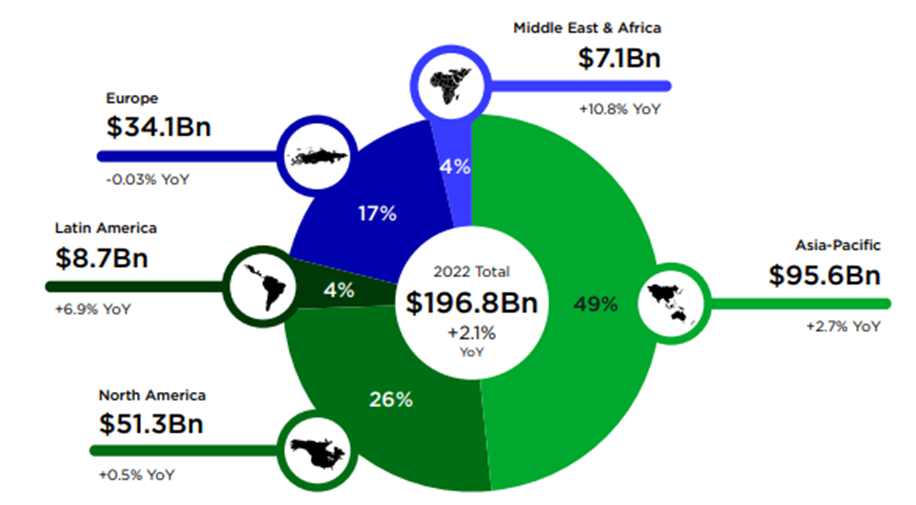

Geographically, the largest proportion of revenue is generated from the Asia Pacific (Japan, South Korea and China), while mobile-first markets such as Middle East & Africa have advanced the most over the year.

Source: Newzoo

Investors can gain exposure to this secular growth theme via Australia’s first dedicated, and most cost-effective video gaming and esports ETF, the VanEck Video Gaming and Esports ETF (ASX:ESPO). ESPO also presents technology diversification away from the FAANGM stocks – Facebook, Amazon, Apple, Alphabet, Netflix and Microsoft.

Key risks

An investment in the ETF carries risks associated with: ASX trading time differences, emerging markets, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS for details.