What is behavioral bias?

When people make irrational decisions, it’s probably because of some human biases they have. These unconscious errors in our thinking can influence everything from the food we buy to the investments we make. Every day, behavioral bias has a huge impact in the world of finance. You might also hear it referred to as cognitive bias.

What is behavioral finance?

Behavioral finance is the idea that our biased behavior can manifest itself in our financial decisions.

Our biases depend on several factors—like our tolerance for risk, when we need to see a return, and so on. The beliefs we have and the emotions we feel based on past experience will play a big role in the kind of investment decisions we make.

For example, if markets took a sudden tumble, what would your instinct be? You might decide to stop investing until things calm down, or you could panic and start selling. You could also see it as a chance to buy stocks at lower prices. The market event is the same, but your behavior depends on your beliefs.

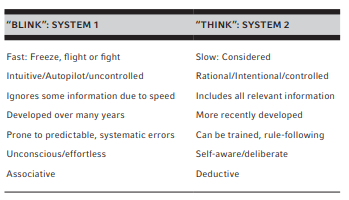

Understanding Blink and how it can hurt your pocket

Our brains make decisions in a world of limited and poor information. They are hard-wired for quick pattern recognition and decisions made on the fly, referred to by experts as System 1 or Blink. This has proved helpful for survival in the wild but is less useful in the world of investing. It can push us toward patterns that may not actually exist.

Examples of behavioral biases in investment decision making2

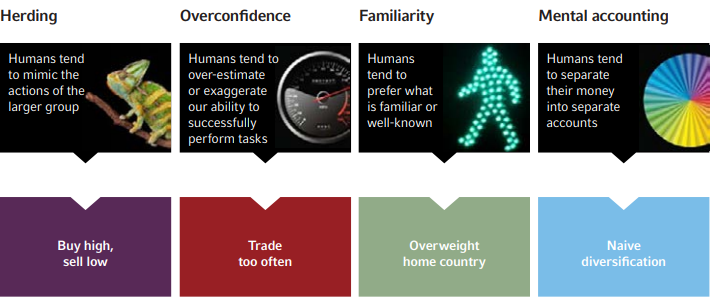

You should buy low and sell high. So why do investors sometimes do the opposite?

Herding biases

We humans tend to follow the crowd. We like to fit in because exclusion from the pack could be dangerous. So, if we see that others are selling, then we are more likely to do the same.

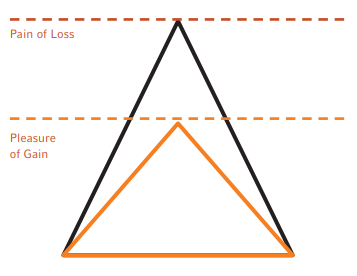

Greed

If we try to squeeze every penny of profit from an investment, it could mean holding on to it after the market has peaked. Greed could also mean chasing the success of others and buying at a higher price.

Fear

We often fear failure more than we desire success.3 This aversion for losses could drive us to selling in a bear market—even if the investment still makes sense over the long-term—or missing out on new buying opportunities entirely.4

Overconfidence

If a person has succeeded in the past, they might try and chase that past performance over and over. For instance, our study shows that the investors’ inclination to chase past performance cost them 1.8% annually in the 34-year period from 1984-2017.5

Home bias

We very often prefer what is familiar. This is especially true for investors who tend to keep their money in the country or region they live in. This reduces diversification opportunities.

Naive diversification

Who doesn’t love a simple solution to a complicated problem? Sometimes we make lazy attempts at diversification—like simply keeping our money in separate accounts.6This can leave us badly exposed when markets take a tumble.

How to avoid behavioral bias

We all have biases, but we don’t need to act on them. By understanding what your biases are, you can learn how to avoid them when making investment decisions. By following a robust long-term strategy instead of your unconscious whims, you’re more likely to achieve your financial goals.

1 Source: “System 1” and “System 2” terminology taken from Daniel Kahneman, Thinking Fast and Slow.

2 Multiple biases may contribute to some particular investor behaviors and investment strategies.

3 Source: Advances in Prospect Theory – Cumulative Representation of Uncertainty, Tversky and Kahneman, 1992.

4 Also related to regret aversion bias: fear of bad outcomes and desire to avoid blame for poor result, e.g. fear of missing out on fads or stay out of market to avoid downturn.

5 BNY Mellon Analytical Services, Russell 3000® Index annualized return from January 1, 1984 to December 31, 2017.

6 For example, a cash account for basic expenditures, a growth shares portfolio to fund education needs or vacation, a conservative bond portfolio for retirement needs.