Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP, discusses the cash rate.

- The RBA left the cash rate at 4.1%. This followed a 0.25% cut in February.

- However, the RBA noted that it is “cautious about the outlook”, but its overall commentary appears a bit more dovish than was the case after its last meeting.

- We expect the RBA to cut again in May and August taking the cash rate to 3.6% this year with another cut next year.

- This should help underpin a modest further pick up in Australian economic growth to around 2%yoy.

RBA holds as it awaits more confidence that inflation will continue to fall

As widely expected, the RBA left its cash rate at 4.1%. In doing so the RBA noted that while underlying inflation continues to ease in line with its forecasts it “needs to be confident that this progress will continue.” More broadly it noted that weakness in demand in some sectors makes it difficult to pass on cost pressures, wage pressures have eased a bit more than expected and global uncertainty remains high on the back of US tariffs, but it also notes that the labour market remains tight, productivity growth has not improved and private demand appears to be recovering.

Put simply there has not been enough new information to further add to confidence that inflation is sustainably returning to the mid-point of the 2-3% target range. So it left rates on hold.

While the RBA won’t say it, being in in the midst of an election campaign was another good reason to leave rates on hold with the RBA preferring to avoid being drawn into the campaign as far as possible – not that it would have been the deciding factor anyway and we do know from the past that if the RBA feels a need to move it will do so in election campaigns but that clearly wasn’t the case this time.

RBA guidance remains “cautious about the outlook” for inflation and presumably future rate cuts, noting again that there are “risks on both sides” for inflation. As in February it still appears concerned that if it eases too quickly inflation could settle above the mid-point of the target range.

However, the RBA’s guidance appears to be a bit more dovish than was the case in February with the post meeting statement removing references to a further tightening in the labour market and the risks around easing “too much too soon” and dropping an explicit reference to caution “on prospects for further policy easing”. And it now looks to be more concerned about the impact of US tariffs particularly if they are widened – as appears certain – on global activity. And RBA Governor Bullock did not appear to be pushing back as much against market expectations for further easing as was the case in February, just saying they will have another look at it in May and that its forecasts are “uncertain”.

As in February the RBA repeated that it will “rely upon the data and the evolving assessment of risks”.

Source: Bloomberg, AMP

We continue to expect the RBA to cut again in May and August

The RBA’s caution is understandable as after the experience of the 2022-23 it doesn’t want to be blamed for causing another surge in prices because it eased too quickly.

However, we continue to see further rate cuts ahead as we see economic growth picking up more slowly than the RBA is forecasting and slowing wages growth will cool sticky services inflation likely taking underlying inflation back to the mid-point of the target range earlier than it expects.

- Yes, unemployment is historically low at 4.1% but there is no sign of a wages breakout with wages growth slowing implying that the non-accelerating inflation rate of unemployment (NAIRU) is likely lower than the RBA’s assumed 4.5%.

- As the RBA notes, monetary policy is still restrictive. February’s 0.25% rate cut reversed just one of the 13 rate hikes between May 2022 and November 2023 which totalled 4.25%. For mortgage payments it reversed only about 8% (or $1300) of the $16,300 increase in annual payments on a $660,000 mortgage since May 2022.

- Trump’s still escalating trade war adds to uncertainty but absent any retaliatory tariffs by Australia which the PM has said it will not do or a plunge in the $A, the tariffs pose more of a downside threat to Australian growth than an upside threat to inflation and so add to the case for cutting rates.

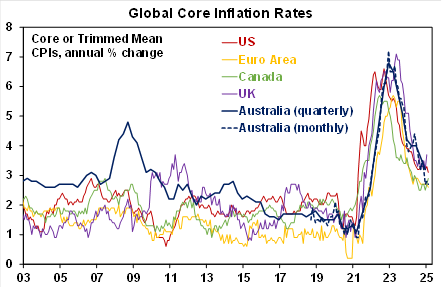

- Partly based on monthly inflation data to February we expect that March quarter inflation data will confirm a further leg down in trimmed mean, or underlying, inflation to 0.6%qoq or 2.8%yoy, down from 3.2%yoy in the December quarter. This would be below RBA expectations for a 0.7%qoq rise.

Our assessment is that the 20 May meeting is “live” for another cut with the key being the March quarter CPI due 30 April, developments around Trump’s escalating tariffs and the RBA’s revised forecasts. With trimmed mean inflation likely to come in below RBA forecasts, the trade war likely to escalate and the RBA likely to revise down its underlying inflation forecasts we expect another 0.25% rate cut in May.

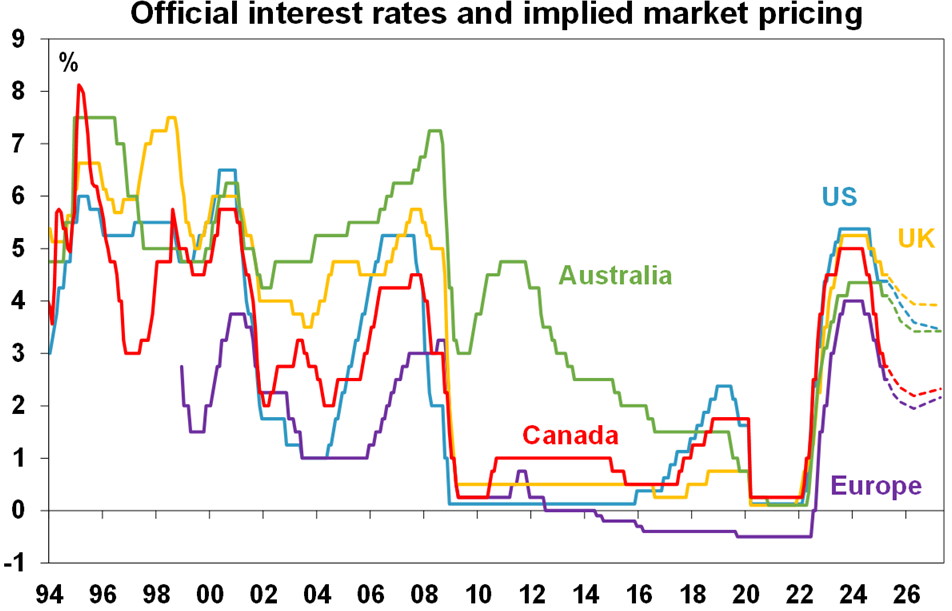

Beyond that we expect another cut in August, taking the case rate down to 3.6% with another rate cut early next year. In support of further rate cuts, underlying inflation in Australia is now in line with other countries which are cutting rates with the December monthly trimmed mean rate of 2.7%yoy similar to core inflation in Europe and Canada, which have cut rates well below the RBA’s cash rate.

Source: Bloomberg, AMP

Ends